WM2NS trade ideas

Nothing Changes - The Next Mortgage CrisisWe all know it's going to happen, just a matter of when, it seems.

Day after day, I come across different traders who have their own narratives about when this debt crisis will finally rear its ugly face and we will be faced with a sober reckoning of decades of monetary irresponsibility and irresponsible allocation of scarce resources to state capitalist companies that veer further and further away from sensible business decisions. Some of us seem to think that it is right around the corner, and that we've got to stack gold, silver, and/or bitcoin to prepare ourselves. Others believe that it's just a deflationary downspiral from here. Most of us seem to be inbetween.

For me, I think it is pretty easy to see. And though my indications would otherwise be seen arbitrary or even nebulous, I think there are some important facts that we have to make clear so that the future isn't as unclear.

The first thing I want to bring to everyone's attention is the growing mortgage-backed securities (MBSs) owned by the Fed, and what this means, put simply, for the rest of the economy and our private banks.

After the pandemic scare, among everything else dropping, one thing didn't see a drop, but a stark, parabolic rise: MBSs owned outright by Federal Reserve Banks. We saw a nearly 30% rise since mid-march:

fred.stlouisfed.org

A rise, which had been seeing a gradual, but steepening, fall since February or March of 2018.

This means two things:

1. Creditors who owned these MBSs held little faith that they could make passive income from the interest off of these MBSs, and sold them to the highest bidder (always the good ole ' Fed).

2. Creditors, also, had little faith in the outlook for these MBSs since any hope for rising interest rates were put to an end, and the narrative that they will be higher doesn't seem to be coming back for a long time. In my opinion, these hopes will never come back.

So how does this affect the banking sector? There's no way they can compete with the Federal Reserve, at this point. If you are inflationary about the future, then you will understand that the Federal Reserve is very deadset on making sure no bubble pops. They will do this by buying up all the debt that they can to avoid default. Unfortunately, this doesn't last forever, and at some point, the Fed is guaranteeing the debt of the whole country, and banks cannot compete with the ultimate market maker and the ultimate currency-producer. For debt-ridden, irresponsible Americans, it will be a wolf in sheep's clothing that seems like a Godsend as every bit of their debt is turned into an asset by the Fed, and even further, as the dollar continues to be debased and "realligned", they will see a steep drop in the strength of their buying power. That's what happens when all of your manufacturing and resources have been imported for decades, and a majority of your skilled workers are foreignborn who have an easy ticket back home where it is much less zany.

I think it is a joke to be deflationary with facts like this. The one needle of deflation in the inflationary haystack is that GDP will slow, and the Fed and Congress will be powerless to stop Americans from saving and paying off their debt, which would be a fair point, if every bit of info was against this. Americans are still the worst savers, incredibly indebted, and will look to any handout that they can get. I think the inevitability that negative interest rates are coming will end up benefitting Americans in the mediumterm.

Negative interest rate policy, NIRP, will be a reckoning for Americans' lifestyle, that will whither down to look much similar to those in Cuba or Albania during communist rule. Debt will be basically turned inside out into credit, and your debt will be used as a backing to the currency. The more you spend, the better. Anyone who has read about government cryptos and NIRP/ZIRP will understand this. Our monetary system will be backed by debt, much like it already is, but the velocity will be kept up so high that in order to maintain your standard of living, you will have to keep purchasing. Put simply, every month you'll get however many dollars, and there will be a timer on it that will expire after however much time, and you will have to spend it all, or it will disappear. Much like vacation days at a lot of your jobs at the end of the year.

Now why would we take a step in this direction? It's only because the Fed and gov't have all interest to do so. Sure, all of our standard of living will diminish, but the Fed will be heroes and be seen as the saviors who helped uphold American lifestyle while the greedy companies tried to steal from us. Everything is in their favor - the government and government-owned media control the placement of the Overton Window.

So to clarify, the main reason the Fed will inevitably be the last bank standing will only be due to the fact that they will do everything they can to stop this Everything Bubble from popping, and will gradually, own every bit of debt out there, and have to rely on NIRP to keep anyone from defaulting. The average American, who can't even tell you where France is on a map, or who Robespierre was, will laud NIRP because it allows them to maintain whatever leveraged lifestyle they've been maintaining for decades, without any attempt at saving or financial planning.

www.cnbc.com

Americans raiding retirement savings to avoid defaults and to stay afloat.

www.marketwatch.com

"One-third of homeowners have less than $500."

"25% of Americans have no emergency savings... 16% have taken on more debt... nearly 1/3 report having lower income than at the start of the pandemic."

"Some 95% of workers in low-income households — making less than $36,000 per year — have either been laid off as a result of the coronavirus (37%) or have experienced a loss in income (58%). A quarter of workers earning between $90,000 and $180,000 a year saw an income loss."

This is a huge point that deflationists and inflationists alike will use to push their narrative, but only the inflationists are right when it comes to how the Fed will act. Sure, the initial onset of Americans jumping into the dollar is a magnificent tailwind for the DXY, but the Americans who have to endure a new loss of income who are extremely frustrated with how things are going, in tandem, with politicians who are steadfast in trying to bring whatever relief will not bide well for deflationists. We either see growing unemployment, growing social unrest, and everything under the sun that is perfect for a violent revolution and exponential drop in standard of living, or we see what we've been seeing for years - Fed and gov't action to maintain status quo and freebies for as long as their fake currency can stand it.

So as unemployment stays steady, standard of living sees a drop, and more Americans save, there will be more of a rush for the Fed to take action and prop up what corporations they can and back whatever debt possible to keep the rusted, empty freight-train rolling at mach speeds.

And in short, the markets see no signs of dropping. We might see another big drop soon as people draw from their pensions and 401ks, but technical indicators see further moves up for the major indexes. The time for a big drop is now, and it just hasn't happened - not as violently as many of us initially thought. Going short is a good way to get screwed super quick in a bubble that is everinflating.

How is the FED handling the ongoing crisisM2, a measurement of the money supply, is a critical factor in the forecasting of issues like inflation. Inflation and interest rates have major ramifications for the general economy, as these heavily influence employment, consumer spending, business investment, currency strength, and trade balances. In the US, the Federal Reserve publishes money supply data every Thursday at 4:30 p.m., but this only covers M1 and M2. Data on large time deposits, institutional money market funds, and other large liquid assets are published on a quarterly basis and are included in the M3 money supply measurement.

This century alone, M2 has been growing. In each of these years; 2001, 2008, 2011 and 2020, the Fed pushed it a notch higher. These years coincide with periods of economic weakness.

So, how has the Fed reacted this year?

First, it's important to understand that the Fed's dual mandate is to manage unemployment and inflation.

Interest rates

The Fed has lowered interest rates as it did back in 2008. This has lowered the cost of borrowing.

Paycheck Protection Programme

In accordance with the CARES act, the Fed started a program that enabled businesses to keep paying their employees. This has helped reduce unemployment from 13.3% in May to 7.9%.

Main Street Lending

Five facilities have been setup for lending to businesses and NGOs.

Treasury Securities

The Fed ramped up its purchases of Treasury securities. It bought around $1.7 trillion worth between mid-March and the end of June. The Fed also increased its purchases of mortgage-backed securities. In general, the Fed’s purchases of securities keep markets working when assets are otherwise difficult to sell. The purchases also inject cash into the economy, and convey to the public that the Fed stands ready to backstop important parts of the financial system.

Therefore, as the situation evolves, this would be a good time to study the market in relation to Fed actions. I believe more volatility is going to be experienced during the northern hemisphere winter season. The Fed, ECB, BOE, BOJ and other central banks are reacting differently and this will impact your trading. Be on the look out for news regarding central banks around the world.

Correlation between M1 and M2-M1There are lot's of people claiming that an expansion of the balance sheet ( M1 ) does not lead to an inflation of the monetary supply ( M2 ) since the additional reserves created by the Fed can't be spent by the primary banks that receive them. This does not take into account the fact that there being less debt instruments after the purchase (yet the same amount of currency) will create appetite in the market for companies to issue new debt, leading to an expansion of M2. Additionally, in the future the primary banks could use those increased reserves to lend more money into the market if/once the appetite for borrowing increases and interest rates increase. To see whether there's a correlation we compare M1 (e.g. cash & reserves) with M2-M1 (broad money supply minus cash & reserves).

How to collect TradingView Coins and refer your friendsIn this video, we show how you and your friends can collect $30 in TradingView Coins to use toward paid plans like Premium. If you refer TradingView to a lot of people, make sure to follow this video closely. It's how you and your network can get $30 worth of TradingView Coins.

Step 1 - Visit the refer-a-friend page where you can find your unique link. You can find the refer-a-friend page in your menu or by using this link.

Step 2 - Copy your unique link and share it with your friends, colleagues or network. Your unique link can be shared as a tweet, Facebook post, email or text message. If you run a blog or website, you can also place your unique link there.

Step 3 - When someone signs up for a paid plan using your unique link, you will both receive $30 in TradingView Coins.

Step 4 - Your TradingView Coins can be used toward a paid plan. A single coin is equal to $0.01. When someone signs up for a paid plan using your link, you will both get $30 in TradingView Coins to use toward Pro, Pro+ or Premium.

Step 5 - You can also donate your coins to other users. For example, when you visit our profile page here , at the top right, there's a button that says Donate . Click that button if you think our ideas are awesome and send us some coins! We just may do the same for you. 😉

We hope you enjoyed this video and that you collect some TradingView Coins using your unique refer-a-friend link. If you have any questions, please write them in the comments below so our team can help.

The myth of hyperinflation series #5- Velocity of moneyEven if the purchasing power is rising, without the increase of velocity of money, there will be no inflation and sustained economic growth.

Circulation/velocity of money measures the interval between money transactions, decline means less transaction is taking place and the interval between money transactions is getting longer.

According to the July 2020 Senior Loan Officer Opinion Survey on Bank Lending Practices, senior loan officers have tightened their standards and terms on commercial and industrial (C&I) loans to firms of all sizes. Furthermore, banks reported weaker demand for C&I (commercial & real estate) loans from firms of all sizes and weaker demand across all three major commercial real estate (CRE) loan categories- construction and land development loans, nonfarm/nonresidential loans, and multifamily loan over the second quarter of 2020.

Next, we will look at demand and consumption.

The velocity of money is plunging so let's make some coin off itHardly surprising though, this has taken place whenever GDP contracts & unemployment increases as it certainly will this year. I think one would suspect that this could lead to risk of deflationary effects - which I know sounds odd when one thinks and sees first hand the rampant money printing and radical expansion of money supply, and inflation increasing. I am still heavily biased towards inflation arising over the next few years, with rates eventually rising to combat inflation - but I do want to be on the lookout for any hints as swiftly as possible that my ideology may be wrong.

I suspect this drop within the velocity of money is especially pronounced in hospitality industries, restaurants, hotels, aerospace, airlines, tourist destinations - where capital is not being exchanged as freely. We also have unemployment up so some individuals simply are being much more wary of purchasing wants, with potential needs still needing to be met on the horizon.

I think mfg's as well have had supply issues coupled with demand issues, with inventories only now ramping back up. With the low demand, and low supply this is a sour recipe that creates less opportunities for transactions, again hurting the velocity of money.

What does all of this mean? I think one needs to carefully weigh the proper strategies in the event inflation or deflation where to occur. In the event of the dreaded stagflation again, the writing will be more clear if that is to occur, but again we need to plan accordingly and develop strategies for each.

A simple strategy I am doing even outside of the fixed income corporate debt/Div yield strategies etc is within actual real estate.

If one were to acquire a home in this environment and inflationary affects play out, you essentially get to double dip on the inflationary affects in a favorable manner. the devaluation of the dollar will be an effect of the inflation. What does this mean for your mortgage?

The dollar amount of the debt side of the mortgage will decrease in value, relative to the purchasing power of the dollars within the debt. The debt itself gets eroded away from inflation. Very favorable if you have debt.

We want equity with debt of course though. And much more equity relative to the volume of debt. The equity of the home will actually be continuing to rise because the value of dollars continuing to loose value will require more dollars to purchase the same amount of equity - meaning the equity increases in terms of dollars.

So inflation will result in the loan decreasing in a dollar weighted comparison, while the equity in the home will increase because of the dollar's devaluation.

Equity relative to a home is one thing, but this comparison can be made with equities (stocks) as well, but I think the home comparison may be helpful in getting my logic communicated clearly.

Again, this does not mean to go wild longing equities - just like you do not want to go wild and start buying junk houses in the middle of Antarctica

We need to be tacticians with finesse

***If you have a great strategy please be sure to share it with me.***

Every time M2/Silver RSI hit these levels S&P500 had a setbackEvery time the M2/Silver ratio RSI hit these levels S&P500 had a setback. Will this time be different?

So is the printing over?July seems to indicate the first monthly decline in M2 in many years. Is the Fed reigning things in?

20% Increase in Currency Supply in 4 months!Just making an observation that the total amount of currency in circulation (Physical + Bank Credit) has increased an unprecedented 20% in the last 4 months. I believe, when we are looking at this chart, we are looking at a Credit Bubble.

Something that bothers me. Current National Debt is around $24.2T, however, we have $18.4T in total dollars in circulation. So even if you use every dollar in existence to pay off the National Debt, you still have $5.8T USD in debt remaining... how does that get paid off?? Need to dig more into this.

Going flat for nowWith States closing back down and talk of more stimulus checks. How long will this stay flat. The narrative to print whatever is needed has not changed. No way to know exactly what will happen just have to watch.

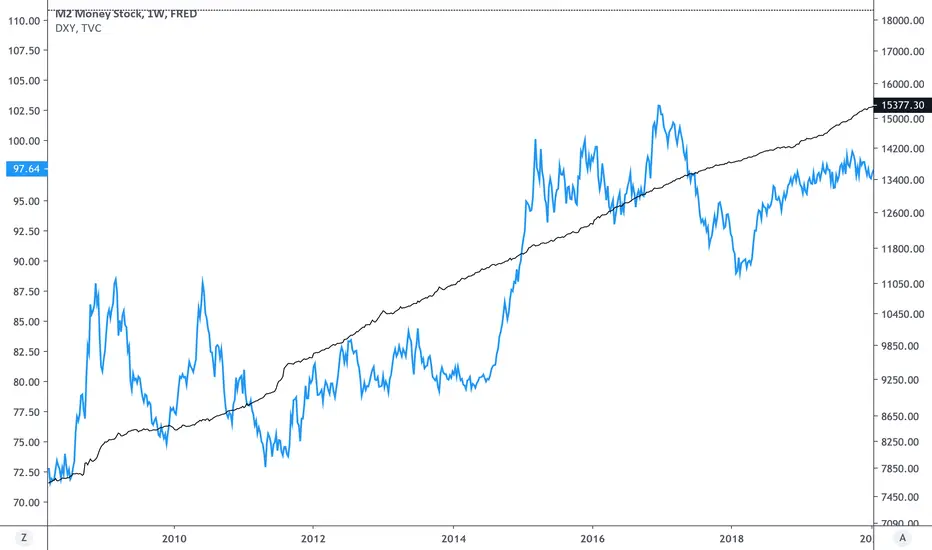

Dollar goes up when M2 money stock goes upBLATANT FED MANIPULATION! OBVIOUSLY THE DOLLAR GOES UP WHEN THEY PRINT MORE LOOK AT THE LINES THEY BOTH GO UP AT THE SAME TIME!

Help me, FED Printer. You're my only hope.With S&P 500 closing on the 50 weekly MA. Markets are standing on the edge. All time highs are still totally possible if public sentiment allows for more printing. Months ago I suggested a possible crazy crash in DJI it's far for a certain reality though I found it eye opening to downside potential. I have linked it below. I am relatively neutral on market direction FED influence is to impact. Volatility is still high enough that stop positions could have a lot of downside risk. Looking at hedge strategies to cover those losses. Any suggestions welcome.

Overpriced Tech vs Undervalued Travel StocksThe Fed has been pumping up market with free cash since pandemic crash, which already been flatten up recently. And the market is acting irrationally piling up tech stocks way more than the available money supply, while leaving travel stocks undervalued. All technology stock such as TSLA, AMZN, AAPL, GOOG, MSFT, etc. are unreasonably overpriced. While all travel related stock such as airlines BA, AAL, DAL, LUV; cruise line NCLH, RCL, CCL; resort: LVS, MGM, PK etc and some banks JPM, BAC, C, etc are left undervalued. Market are recovering steadily, business are opening up, people are start to traveling out, especially in the country that has recovered from pandemic. Data from flight radar shows that domestic flight is recovering steadily. Peoples has forgotten DotCom crash and leaves many tech stock drop more than 80% and need a decade to recover. The market will reverse soon and in the long run the travel stocks has more upside potential.

www.flightradar24.com

Money stockyou know something is fucked up when even in the log chart you notice an exponential increase

Cash is King, Bull run incoming! M2 includes a broader set of financial assets held principally by households. M2 consists of M1 plus: (1) savings deposits (which include money market deposit accounts, or MMDAs); (2) small-denomination time deposits (time deposits in amounts of less than $100,000); and (3) balances in retail money market mutual funds (MMMFs). Seasonally adjusted M2 is computed by summing savings deposits, small-denomination time deposits, and retail MMMFs, each seasonally adjusted separately, and adding this result to seasonally adjusted M1

With this increase in cash flow & asset holding, I wouldn't expect a bear cycle anytime soon!

Price Level is WHACKMoney Supply ( M2 ) x Velocity of Money ( M2V ) = Price Level x real GDP ( GDP )

Therefore

Price Level = ( Money Supply ( M2 ) x Velocity of Money ( M2V ))/ real GDP ( GDP )

All I did was graph the Price Level according to the first equation

SPX vs M2 will it continueLooking at the M2 charts the the money printing seems to be slowing a bit still at a rate of over 8% per year. Comparing these to i'm considering 3 factors of what could be next.

1. Deflation stock market crashes and value floods into the dollar with another mass sell off. Looking for weakness in S&P as the printing slows.

If deflation happens having USD is ideal.

2.Back to normal M2 money levels off to normal's. The stock market maintains gradual growth, GDP increases. Velocity of money increases and exponential growth in cost of goods is not felt.

If back to normal happens having stocks might could be profitable. The biggest risk being the increase in cost of goods because of velocity of money increase.

3. Hyper Inflation this is least probable to happen next though still very much possible. In that case M2 would need to increase much more.

Cash would be worthless, stocks would be next to worthless though increasing in price daily in relation to uses currency. In this case gold, silver and cryptocurrencies would be ideal.

I think if this were to happen cryptocurrencies would have to compete with gold and silver to see which is better money.

USD in troubleThe numbers seem to indicator we are now at 17% inflation of M2 this year. It's just getting faster. It's likely May ends at 20%. If you don't understand why markets don't reflect this please read my post Can't feel inflation yet I linked it at the bottom. At this rate by next September M2 inflation would be equal from start of 2020 till 2021 September and 2008-2020. Based on the currently numbers it's likely to be faster then that. As for the simplicity of the math I calculated staying at our current growth rate. The numbers so the rate increasing unless something changes it will happen faster. Many people think Covid-19 being over might stop this growth though that does not factor time for businesses to start recovering. Also when businesses start to recover and consumer confidence increases so will spending. The velocity of money increasing will mean people start to feel the effects of inflation.

Funny not funnyIt's funny how fast this is going up 16% in the since the start of the year. Sadly most people don't know anything about M2 money or Fed money printing. They will be the victims of this. Though I do believe it's best to not live the victim life. People should be educating themselves rather then blaming others. Regardless it's hard to watch people go rough times. Including the 120 Million people globally predicted by world food program to be at risk of starving due to lock down impacts on economics.

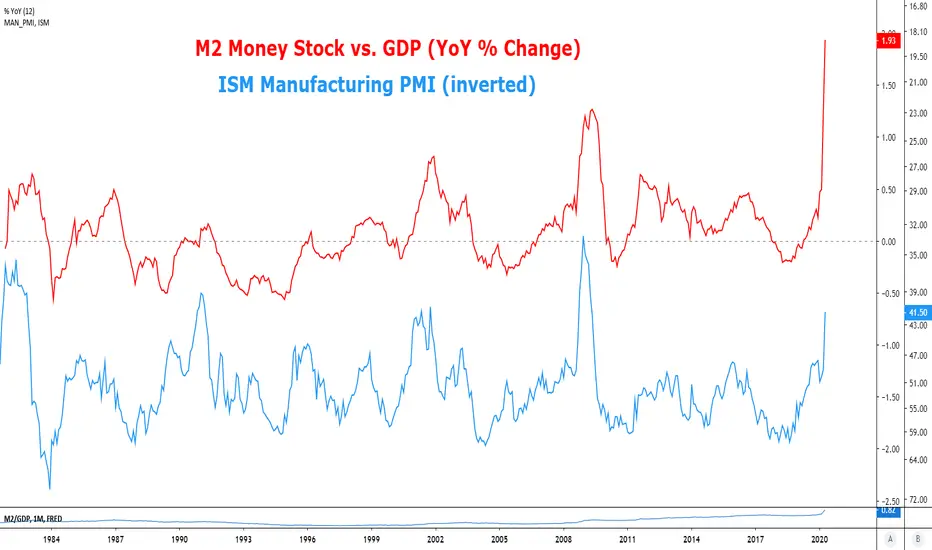

M2/GDP RatioThis ratio is indicating more pain to come from macro indicators such as the ISM Manufacturing PMI..