Euro Soars with Dollar WoesOne thing about tables, they turn. This time last year, the dollar was unrivalled. Now, it is being challenged amid a banking crisis, recessionary fears, and a debt ceiling drama.

Having stepped up on the rates faster than the rest, the US Fed’s combat against inflation fuelled a dollar rally . It now finds itself between a hard place and a rock. Many expect the Fed to pause.

In contrast, the ECB, having been slower off the block, has gradually lifted rates with ample headroom for further policy intervention to fend off a resurgent Euro area inflation.

This paper explores fundamental forces driving a rally in the Euro and the headwinds facing the dollar.

With EUR/USD making a golden cross on March 27th, this case study posits a long position in Euro using the CME Euro FX Futures delivering a 3x reward to risk ratio with entry at 1.1025 and target of 1.17 hedged by a stop at 1.08.

Crushed and Bruised Euro is Fighting Back

2022 was a crushing year for the Euro. Geopolitics plunged Europe into an energy crisis. Bleak prospects plus soaring inflation meant deep recession. The Euro was wounded.

The Euro was dealt another blow as the ECB was slow to lift rates. Key eurozone rates were well below those in the US, as the Fed was all pedal to the metal with unprecedented hikes.

Higher yields in the US attracted foreign funds, boosting the dollar at the expense of other currencies.

Tables turn and times change. Euro's rise is in part thanks to milder European winter. Warmer than normal and prudent energy consumption has kept gas prices in check. The region may well avoid a recession. In fact, it posted a surprise output growth in the final quarter of last year.

A hawkish ECB also well supports the Euro. It continues to hike rates to tackle inflation, which remains stubbornly high.

As rates in Europe rise while those in US stall, the Euro will attract capital inflows from across the Atlantic.

Dollar’s dominance is being challenged

Over the last 10 years, the Dollar Index (DXY) has gained ~25% while the EUR/USD has shed ~19%.

The rotation away from the dollar is underway. Not only Euros, but the dollar has also been losing ground against other majors, including the sterling and the yen.

Easing inflationary pressures should spell victory for the Fed allowing it to tone down its fighting monetary stance.

Premium for insuring against US government default spiked to its highest level in more than a decade amid political impasse related to debt ceiling. While this political embarrassment is likely to be inconsequential, the tiny risk of a dollar debacle cannot be ignored. Investors hedging against this risk are likely to push the dollar lower.

Is this De-dollarisation?

The de-dollarisation camp shouts loud. But ignore the noise.

Surely, the weaponisation of the dollar has alarmed nations. Not surprisingly, many are attempting to wean away from dollar dependence for trade settlement.

The dollar’s share in forex reserves used to be 71.5% at the turn of the century and has gradually declined to 58.3% as of the end of 2022.

The dollar remains at the core of global trade and finance. The dollar forms 88% of FX transactions. Distant second is Euro at 31%, according to 2022 BIS figures (aggregates equal 200% as each transaction involves two currencies).

Transactions involving the Chinese yuan having grown at 70% over last three years represents a mere 7% of the total.

About 60% of the world's forex reserves aggregating to USD 11 trillion are still denominated in dollar.

The dollar will continue to play a pre-eminent role in global trade and as a global reserve for a long time to come. Absent a credible alternative, albeit weakened, the dollar is here to stay.

Rate Expectations Point to the Fed Pausing Earlier Than ECB

CME’s FedWatch tool shows a 78% probability of another 25bps rate hike at the next meeting on May 3rd and a 67% probability of no rate hike at the June meeting. Fed pause before pivot remains market expectations.

Meanwhile, Reuters reported that the ECB is expected to raise rates by 25bps at its next meeting in May. Crucially, ECB survey of professional forecasters points to another 25bps rate hike in Q2 before pausing.

Asset Managers & Funds are positioning for Euro to rally

CFTC’s Commitment of Traders (CoT) report shows that leveraged funds and asset managers are bullish Euro. Asset managers increased net longs by 7.4% over the last 12 weeks. Leveraged funds have flipped from net short to net long, increasing long positioning by 125%.

Meanwhile, the CoT for DXY futures shows that asset managers are still net long but have reduced long positions by 20.5%.

Options Market are signalling bullish Euro and bearish Dollar

Monthly options on Euro FX futures are trading with a put-call ratio of 0.87 pointing to more calls than puts, indicating Euro bullishness. Euro buoyancy is particularly apparent for June expiry options which have a put-call ratio of 0.6.

Meanwhile, thinly traded options on DXY futures expiring in June have a put-call ratio of 1.66 signalling that market participants are bearish dollar with 1.66 puts for every call option.

Trade Setup

Each lot of CME Euro FX Futures provides exposure to 125,000 Euros. Every 0.00005 increment in the contract represents a trading P&L of USD 6.25.

● Entry: 1.1025

● Target: 1.17

● Stop: 1.08

● Profit at target: USD 8,440

● Loss at stop: USD 2,810

● Reward-to-risk: 3x

MARKET DATA

CME Real-time Market Data helps identify trading set-ups and express market views better. If you have futures in your trading portfolio, you can check out on CME Group data plans available that suit your trading needs www.tradingview.com

DISCLAIMER

This case study is for educational purposes only and does not constitute investment recommendations or advice. Nor are they used to promote any specific products, or services.

Trading or investment ideas cited here are for illustration only, as an integral part of a case study to demonstrate the fundamental concepts in risk management or trading under the market scenarios being discussed. Please read the FULL DISCLAIMER the link to which is provided in our profile description.

M6E1! trade ideas

simple trading rule: stay long near tripple topson the first top exit, also on the tripple top exit but

on the 3rd or 4th time a market goes to new recent high, assume it will break out to the upside...

EUR/USD's hidden clues & key levels?

Here’s an interesting chart: the inflation differential of the US and the EU plotted against the EUR/USD pair. If we approximate the range of the inflation differential with an upper bound of 1.5 and a lower bound of -0.5, we get a compelling signal for trading the EUR/USD pair. Buying EUR/USD when the inflation differential bottoms has resulted in success 4 out of the 5 times this signal was triggered.

Repeating the analysis using the preferred inflation measures for both central banks – PCE for the Federal Reserve (Fed) and EU HICP for the European Central Bank (ECB) – yields similar results.

Is this spurious correlation or is there more to this? Our guess is that the inflation differential drives expectations of one central bank’s move versus the other which affects the currency pair.

The upcoming US PCE release on 28th April will provide insight into whether the inflation differential between the US and EU will continue to narrow. The validity of this data remains to be seen, but it's certainly an intriguing observation to consider!

The rather eventful economic calendar over the next two weeks offers opportunities for this pair. Starting with the PCE Price Index released on April 28th, it is followed by the Fed meeting on Wednesday, May 3rd and the ECB meeting on Thursday, May 4th.

With these events in mind, we want to position ourselves for the flurry of announcements coming out, which could play into EUR/USD strength.

The long-term price action still seems to point towards an uptrend, with the 100-day Simple Moving Average (SMA) crossing the 200-day SMA and clearly marking previous swings. The current price is also consolidating at the 1.1000 psychological level, with parity and 1.2000 levels roughly marking the EUR/USD range for the decade.

Zooming in, the EURUSD has been trading in an uptrend. An attempt to break above the 1.11 level was quickly rejected, with prices trading back to the trend support shortly after. We are currently witnessing another attempt to break this same level once again. Hence, a risk-managed trade could yield opportunities here with the upcoming onslaught of announcements. Setting up a long position at the current level of 1.1074 with a tight stop just below the trend support at 1.0945 and take profit level of 1.1400 would give us a risk-reward ratio of roughly 2.5. Each 0.00005 increment per EUR in the EURUSD futures contract equal to 6.25$.

The charts above were generated using CME’s Real-Time data available on TradingView. Inspirante Trading Solutions is subscribed to both TradingView Premium and CME Real-time Market Data which allows us to identify trading set-ups in real-time and express our market opinions. If you have futures in your trading portfolio, you can check out on CME Group data plans available that suit your trading needs www.tradingview.com

Disclaimer:

The contents in this Idea are intended for information purpose only and do not constitute investment recommendation or advice. Nor are they used to promote any specific products or services. They serve as an integral part of a case study to demonstrate fundamental concepts in risk management under given market scenarios. A full version of the disclaimer is available in our profile description.

Reference:

www.cmegroup.com

EURUSD Short-Term AnalysisThis expectation is a framework to look for a potential trading setup; I don't just execute based on these levels, I always wait for confirmations on lower timeframes

This Analysis was done using my complete Strategy which includes:

- Smart Money Concepts

- Multi Timeframe Liquidity and Market Structure

- Supply And Demand

- Auction Theory

- Volume Analysis

- Footprint

- Market Profile

- Volume Profile

- WYCKOFF

- ETC

6EM3 High: 1.1066 Low: 1.0895 SidewaysWeekly Kickoff levels are longer timeframe levels where we believe longer time traders will adjust inventories.

6EM3 High: 1.1100 Low: 1.0880 HigherWeekly Kickoff levels are longer timeframe levels where we believe longer time traders will adjust inventories.

6EM3 High: 1.1100 Low: 1.0841 HigherWeekly Kickoff levels are longer timeframe levels where we believe longer time traders will adjust inventories.

6EM3 High: 1.1100 Low: 1.0780 HigherWeekly Kickoff levels are longer timeframe levels where we believe longer time traders will adjust inventories.

IS euro telling the FUTURE of the Market? $6EMLooking at the Euro Futures, looks like the market is battling its impact on the market. The more it drops the more the market drops. I am looking that this testing some levels to end the week in a direction.

What looks like a bear flag is starting to look over extended. We are at what could be a pivot point on the next quarter direction.

Bullish Case - Look we have already above the 50EMA and we are holding that so at best it could retest. DOUBT IT. We above the 0 line on the CCA Swing. Since this is a consolidation zone I am looking for it to do it again as the market builds their position to explode to the upside.

Bear Case - Lets be serious, why would a lower high have any upside left? We already broke the uptrend that started mid March so why chase. The 50 and the 200 has not cross for a while. TIME TO GO... Bearish below 1.087 makes sense. With enough strength we can test the 200 EMA again then fall.

euro🎯 Dollar is reversing in the same moent when euro hit the ob, I think it can go down from here

🟧Entry basics

Never enter blindly on the level. Always put everything in a higher timeframe context. The level must be violated and the price has to do a pullback and Break of the structure. Then you look for the entry on the order block or FVG above/below 50% pullback. SL is above swing high and set TP to 3R. Don't try to predict where the price will go next or don't try to take 1:50R trade. We trade intraday reversal and reaction on the level. We get our 3R and get out of the market.

For the short trade, the scheme would be obviously an upside-down picture picture

🟩When to enter the trade

Setup and entry must occur at these times, as it's the time when we can get the biggest volatility and highest probability

🔵London Session - 02:00-05:00 NY time // 08:00-11:00 EU time

🟢New York Session - 07:00-10:00 NY time // 14:00 - 17:00 EU time

This Strategy is not about predicting the market and the next movements. It's about the trading reaction in the liquidity levels. Which is good enough to make money by trading a couple of hours a week.

6EM3 High: 1.0944 Low: 1.0660 SidewaysWeekly Kickoff levels are longer timeframe levels where we believe longer time traders will adjust inventories.

euro🎯 I will be looking for entries in the external liquidity levels as highlighted on the charts

🟩 Trading TIme

Setups must occur at these times otherwise I'm not interested.

🔵London Killzone - LOKZ 02:00-05:00 NY time // 08:00-11:00 EU time

🟢New York Killzone - NYKZ - 07:00-10:00 NY time // 14:00 - 17:00 EU time

🟧Entry Scheme

Never enter blindly on the level. Always look for the break of the structure and pullback as the scheme shows.

Yes, sometimes the market will not pull back and you miss a trade that's the part of the game. But it's better not to be in the trade you want to be than,

being in the trade you don't want to be.

For the short trade, the scheme would be obviously an upside-down picture picture

🟦 Rules

-Skip the London session if the Asia session was trending

- Wait for manipulation at the session open, which enters HTF POI and takes out Buy-side liquidity/ Sell-side Liquidity

- Look at smart money divergence as the additional confluence

- Wait for Break of Structure ( M1 if in sync with trend / HTF BOS if counter-trend) + displacement/momentum shift M3 /M5 candle close for confirmation

- Figure out: where is your invalidation (SL) and FPOL (TP1) before entering your trade

- Enter short at pullback to first POI (FVG/ OTE /OB) above respective EQ ( discount ) of Return to origin area on lower timeframe

- Set SL above swing low of manipulation, as price already took LQ out it should not go there again.

- When the price moves 50% of the expected Target range, the stop loss can be trimmed by 25%

- When the price moves 75% of the expected range the stop loss can be trimmed to breakeven

- Never trade a POI that has liquidity resting above (short) or below (long),

- Don't enter when FPOL (for example swing low/high) has been hit before getting you into the position

- Never enter a trade right before news events.

- Don't try to predict the market, just take 1:3 RR on the level and get out.

- This is intraday trading but there is no trade every day.

Pick just the best setups. In theory, we have 2 pairs, 2 trading sessions 5 trading days in a week its 20 opportunities.

You don't need to trade them all. With 1:3 RR, making consistently 3 good trades in a week will put you into top 1% class of traders.

🟦Market Maker model Schematics

🟪Smart Money Divergence

The dollar index and USD pairs usually trade asymmetric, for example, DXY making higher highs will result in $EURUSD making lower lows and vice versa. When the price on one has lower lows, it is expected that the other should reach higher highs. When this does not occur, we have smart money Divergence. This is suggestive of major accumulation/consolidation in advance of a major move in the opposite direction.

This is just the basics of my strategy, but enough for you to know what to do on the levels.

👊 BRUCE LEE´S RECOMMENDATIONS:

1 ) “Adapt what is useful, reject what is useless, and add what is specifically your own.”

- Inspired by elements of Market Profile, ICT, and SupplyandDemands strategies I adapted what is useful, rejected useless and added specifically my own parts.

2) “I fear not the man who has practiced 10,000 kicks once, but I fear the man who has practiced one kick 10,000 times.“

- The quote above teaches us about mastery. You don't need to know 5 strategies, tenths of formations, or have 20 pairs on the watchlist. Learn 1 setup pick up 2 pairs and practice them 10 000 times, and become a specialist.

If you have any questions write a comment I'm happy to help

Good luck

Dave FX Hunter

euro🎯 I will be looking for entries in the external liquidity levels as highlighted on the charts

🟩 Trading TIme

Setups must occur at these times otherwise I'm not interested.

🔵London Killzone - LOKZ 02:00-05:00 NY time // 08:00-11:00 EU time

🟢New York Killzone - NYKZ - 07:00-10:00 NY time // 14:00 - 17:00 EU time

🟧Entry Scheme

Never enter blindly on the level. Always look for the break of the structure and pullback as the scheme shows.

Yes, sometimes the market will not pull back and you miss a trade that's the part of the game. But it's better not to be in the trade you want to be than,

being in the trade you don't want to be.

For the short trade, the scheme would be obviously an upside-down picture picture

🟦 Rules

-Skip the London session if the Asia session was trending

- Wait for manipulation at the session open, which enters HTF POI and takes out Buy-side liquidity/ Sell-side Liquidity

- Look at smart money divergence as the additional confluence

- Wait for Break of Structure ( M1 if in sync with trend / HTF BOS if counter-trend) + displacement/momentum shift M3 /M5 candle close for confirmation

- Figure out: where is your invalidation (SL) and FPOL (TP1) before entering your trade

- Enter short at pullback to first POI (FVG/ OTE /OB) above respective EQ ( discount ) of Return to origin area on lower timeframe

- Set SL above swing low of manipulation, as price already took LQ out it should not go there again.

- When the price moves 50% of the expected Target range, the stop loss can be trimmed by 25%

- When the price moves 75% of the expected range the stop loss can be trimmed to breakeven

- Never trade a POI that has liquidity resting above (short) or below (long),

- Don't enter when FPOL (for example swing low/high) has been hit before getting you into the position

- Never enter a trade right before news events.

- Don't try to predict the market, just take 1:3 RR on the level and get out.

- This is intraday trading but there is no trade every day.

Pick just the best setups. In theory, we have 2 pairs, 2 trading sessions 5 trading days in a week its 20 opportunities.

You don't need to trade them all. With 1:3 RR, making consistently 3 good trades in a week will put you into top 1% class of traders.

🟦Market Maker model Schematics

🟪Smart Money Divergence

The dollar index and USD pairs usually trade asymmetric, for example, DXY making higher highs will result in $EURUSD making lower lows and vice versa. When the price on one has lower lows, it is expected that the other should reach higher highs. When this does not occur, we have smart money Divergence. This is suggestive of major accumulation/consolidation in advance of a major move in the opposite direction.

This is just the basics of my strategy, but enough for you to know what to do on the levels.

👊 BRUCE LEE´S RECOMMENDATIONS:

1 ) “Adapt what is useful, reject what is useless, and add what is specifically your own.”

- Inspired by elements of Market Profile, ICT, and SupplyandDemands strategies I adapted what is useful, rejected useless and added specifically my own parts.

2) “I fear not the man who has practiced 10,000 kicks once, but I fear the man who has practiced one kick 10,000 times.“

- The quote above teaches us about mastery. You don't need to know 5 strategies, tenths of formations, or have 20 pairs on the watchlist. Learn 1 setup pick up 2 pairs and practice them 10 000 times, and become a specialist.

If you have any questions write a comment I'm happy to help

Good luck

Dave FX Hunter

euro🎯 I will be looking for entries in the external liquidity levels as highlighted on the charts

🟩 Trading TIme

Setups must occur at these times otherwise I'm not interested.

🔵London Killzone - LOKZ 02:00-05:00 NY time // 08:00-11:00 EU time

🟢New York Killzone - NYKZ - 07:00-10:00 NY time // 14:00 - 17:00 EU time

🟧Entry Scheme

Never enter blindly on the level. Always look for the break of the structure and pullback as the scheme shows.

Yes, sometimes the market will not pull back and you miss a trade that's the part of the game. But it's better not to be in the trade you want to be than,

being in the trade you don't want to be.

For the short trade, the scheme would be obviously an upside-down picture picture

🟦 Rules

-Skip the London session if the Asia session was trending

- Wait for manipulation at the session open, which enters HTF POI and takes out Buy-side liquidity/ Sell-side Liquidity

- Look at smart money divergence as the additional confluence

- Wait for Break of Structure ( M1 if in sync with trend / HTF BOS if counter-trend) + displacement/momentum shift M3 /M5 candle close for confirmation

- Figure out: where is your invalidation (SL) and FPOL (TP1) before entering your trade

- Enter short at pullback to first POI (FVG/ OTE /OB) above respective EQ ( discount ) of Return to origin area on lower timeframe

- Set SL above swing low of manipulation, as price already took LQ out it should not go there again.

- When the price moves 50% of the expected Target range, the stop loss can be trimmed by 25%

- When the price moves 75% of the expected range the stop loss can be trimmed to breakeven

- Never trade a POI that has liquidity resting above (short) or below (long),

- Don't enter when FPOL (for example swing low/high) has been hit before getting you into the position

- Never enter a trade right before news events.

- Don't try to predict the market, just take 1:3 RR on the level and get out.

- This is intraday trading but there is no trade every day.

Pick just the best setups. In theory, we have 2 pairs, 2 trading sessions 5 trading days in a week its 20 opportunities.

You don't need to trade them all. With 1:3 RR, making consistently 3 good trades in a week will put you into top 1% class of traders.

🟦Market Maker model Schematics

🟪Smart Money Divergence

The dollar index and USD pairs usually trade asymmetric, for example, DXY making higher highs will result in $EURUSD making lower lows and vice versa. When the price on one has lower lows, it is expected that the other should reach higher highs. When this does not occur, we have smart money Divergence. This is suggestive of major accumulation/consolidation in advance of a major move in the opposite direction.

This is just the basics of my strategy, but enough for you to know what to do on the levels.

👊 BRUCE LEE´S RECOMMENDATIONS:

1 ) “Adapt what is useful, reject what is useless, and add what is specifically your own.”

- Inspired by elements of Market Profile, ICT, and SupplyandDemands strategies I adapted what is useful, rejected useless and added specifically my own parts.

2) “I fear not the man who has practiced 10,000 kicks once, but I fear the man who has practiced one kick 10,000 times.“

- The quote above teaches us about mastery. You don't need to know 5 strategies, tenths of formations, or have 20 pairs on the watchlist. Learn 1 setup pick up 2 pairs and practice them 10 000 times, and become a specialist.

If you have any questions write a comment I'm happy to help

Good luck

Dave FX Hunter

6EM3 High: 1.0810 Low: 1.0590 SidewaysWeekly Kickoff levels are longer timeframe levels where we believe longer time traders will adjust inventories.

EURO DIXIE SWING-SETUP-

UPPER CHART: 6E1! - EUR/USD Futures (1D)

- 50 Ema (purple)

- Jurik-Filtered, Gann HiLo Activator [Loxx} (green/red)

LOWER CHART: DXY - US Dollar Index (1D) (*Inverse)

- 50 Ema (purple)

- Jurik-Filtered, Gann HiLo Activator [Loxx} (red/green)

From a quick glance at the two charts, it might appear that the bottom chart is simply the same as the top chart but employing Line style instead of Candles.

The bottom chart is actually a DXY Line chart but Inverted (Alt+I) with the HiLo Activator configured with inverse colors.

The correlation is rather astounding. Other US Dollar denominated currencies do not share the perceived precision of this relationship.

The HiLo Activator on a single chart would likely provide similar results. The addition of the inverse DXY simply adds additional input.

-TRADES-

ENTRY - LONG - When 6E1! is above the rising 50 Ema ENTER on a Green flip of the HiLo Activator.

SHORT - When 6E1! is below the descending 50 Ema ENTER on a Red flip of the HiLo Activator.

EXIT - On the following opposite flip of the HiLo Activator.

STOP - When the HiLo Activator flips across Price, it creates a point that it then it moves away from.

That point is rarely exceeded on trades that follow the 50 Ema and is therefore the best Stop location.

Moving Stop into the money too quickly could be hit without flipping the Activator! - Judgement Call .

-NOTES-

FALSE SIGNALS - The HiLo Activator will flip at the point when Price exceeds the calculated HiLo range regardless of the candles status.

A flip is not confirmed until the candle closes. (No repaint after close) - A rejection off the Activator ma can be significant!

- Entry: Wait for the flip to be confirmed on candle close.

- Exit: Waiting for a flip will cost gains! Taking Profits early can miss part of the move. - Judgement Call .

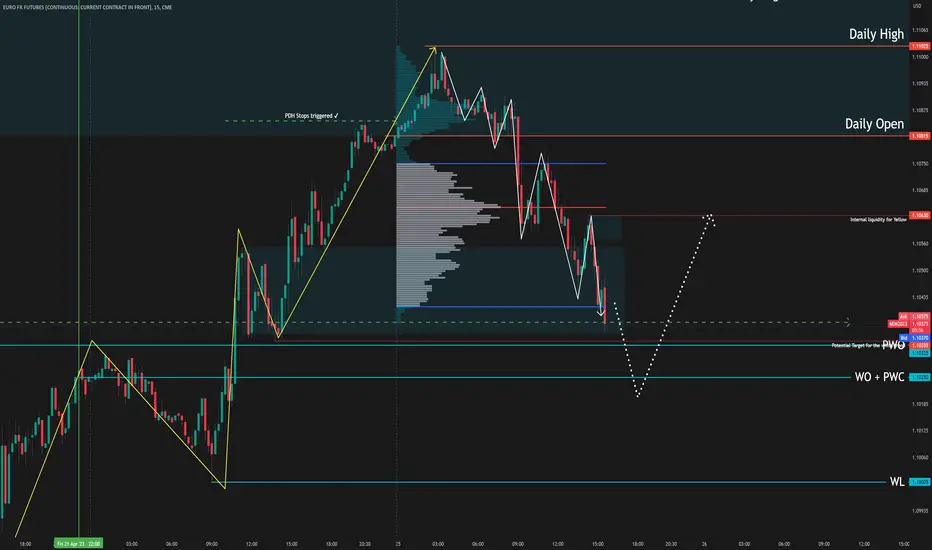

EURUSD Short-Term Bullish Analysis/ExpectationThe price is building liquidity (Equal Highs). The Smart Money might break more structures to the downside to induce sellers before going after the equal highs.

Or it could just take that liquidity without breaking structures first. It will depend on lower timeframes orderflows

Click on Boost (like) to support these free analyses!

This Analysis was done using my complete Strategy which includes:

- Smart Money Concepts

- Multi Timeframe Liquidity and Market Structure

- Supply And Demand

- Auction Theory

- Volume Analysis

- Footprint

- Market Profile

- Volume Profile

- Wyckoff

- Etc.

6EM3 High: 1.0810 Low: 1.0590 SidewaysWeekly Kickoff levels are longer timeframe levels where we believe longer time traders will adjust inventories.

volume spread analysis (VSA) on EURUSDby volume spread analysis

high volume long tail doji candlestick happen on daily demand zone

it show that some big player is try to protect this price area

6EH3 High: 1.0750 Low: 1.0530 SidewaysWeekly Kickoff levels are longer timeframe levels where we believe longer time traders will adjust inventories.

euro futures in strong demandwe are in a strong demand zone we expect the price to react nicely in these zones