S&P 500 LOG Melt-up Top - 6000 - H1 2023H1 2023 Target Top: 6000, followed by the 2nd Great Recession. Top is confluent with our genesis trend-line (Great Depression & Great Recession tops)! Bear Market bottom around 2200 (COVID bottom / 200 Month estimated SMA).

SPX (S&P 500 Index)

S&P 500: Riding the Wave of OptimismS&P 500: Riding the Wave of Optimism Amid Economic and Political Dynamics

The S&P 500 continues its upward trajectory, buoyed by tech-driven gains and investor optimism, even as mixed economic data and geopolitical uncertainties loom. Here’s a deep dive into the current market landscape and what it means for the benchmark index.

---

Economic and Market Drivers

Tech-Led Rally and AI Optimism

The S&P 500's performance has been significantly influenced by gains in the technology and AI sectors. Investors are betting on the transformative potential of AI, propelling stocks like Microsoft and Meta to the forefront. However, regulatory scrutiny, such as the FTC's probe into Microsoft's AI software sales, introduces a layer of uncertainty.

Resilient Labor Market

While the Challenger Layoffs report showed a slight uptick, JOLTS job openings rose to 7.744 million in October, indicating a stable labor market. This balance supports the Federal Reserve’s cautious approach to monetary policy, as Chair Jerome Powell reiterated the economy’s strength and gradual progress in reducing inflation.

Mixed Economic Indicators

- **ISM Services PMI** fell to 52.1, below expectations of 55.7, suggesting a slowdown in service sector growth.

- **Durable goods orders** increased by 0.3%, meeting expectations and reinforcing the narrative of economic stability.

- **Construction spending** rose 0.4%, signaling robust investment activity.

- **University of Michigan 1-Year Inflation Prelim** came in at 2.9% (forecast: 2.7%, previous: 2.6%), showing slightly higher inflation expectations.

- **University of Michigan Sentiment Prelim** reached 74 (forecast: 73.2, previous: 71.8), reflecting improved consumer confidence.

These data points reflect a U.S. economy navigating challenges while avoiding a hard landing—a scenario that fuels investor confidence.

---

Federal Reserve Policy: A Turning Point?

Fed officials, including John Williams and Christopher Waller, have hinted at the potential for a December rate cut, with futures markets now pricing in an **85% likelihood of a 25-basis-point reduction**, up from **67%** before the recent jobs report. Inflation progress appears to have stalled, with Fed Governor Michelle Bowman cautioning that more robust measures may be necessary to meet the 2% target by 2025.

The November jobs report further influenced expectations:

- US Nonfarm Payrolls rose to 227k (forecast: 220k, previous: 12k, revised to 36k).

- US Unemployment Rate ticked up to 4.2% (forecast: 4.1%, previous: 4.1%).

- US Average Earnings YoY remained steady at 4% (forecast: 3.9%, previous: 4.0%).

These figures reflect a labor market resilient enough to accommodate rate cuts, which could provide an additional boost to equity markets.

---

Corporate Highlights

- Salesforce reported Q3 revenue of $9.44 billion, exceeding estimates, but missed on adjusted EPS, reflecting mixed investor sentiment.

- Meta (Facebook) is aligning its strategies with evolving political landscapes, as CEO Mark Zuckerberg seeks to navigate regulatory and policy shifts.

- *Microsoft faces FTC scrutiny, underscoring increasing regulatory challenges in the tech sector.

Despite these challenges, corporate earnings have largely supported market valuations, adding another layer of support for the S&P 500.

---

Seasonality and Sentiment

December has historically been a strong month for the S&P 500, driven by:

- Holiday-driven consumer spending.

- Portfolio rebalancing.

- End-of-year tax considerations.

The Fear & Greed Index, currently at 53, indicates a greed-driven sentiment. This optimism aligns with traders pricing in a higher likelihood of Fed rate cuts, reflecting a favorable market environment.

---

Outlook: Optimism with Caution

The S&P 500’s upward momentum is underpinned by strong tech-sector performance, resilient economic data, and seasonal tailwinds. However, challenges such as geopolitical risks, regulatory scrutiny, and uneven progress in disinflation could temper gains.

The Fed's flexibility and potential rate cuts are positive signals for the market, bolstering growth-oriented sectors. Nonetheless, investors should remain vigilant, monitoring corporate earnings, economic releases, and geopolitical developments.

In the near term, the S&P 500 appears poised to end the year on a strong note. However, with inflationary pressures, mixed economic indicators, and geopolitical uncertainties still in play, the path forward will require a delicate balance between economic stability and investor confidence.

ES Possible Rejection of 6100 and Friday afternoon dumpES looking like it could potentially top out at 6100 and turn back to the downside this afternoon

S&P 500: Riding the Wave of Optimism S&P 500: Riding the Wave of Optimism Amid Economic and Political Dynamics

The S&P 500 continues its upward trajectory, buoyed by tech-driven gains and investor optimism, even as mixed economic data and geopolitical uncertainties loom. Here’s a deep dive into the current market landscape and what it means for the benchmark index.

---

Economic and Market Drivers

Tech-Led Rally and AI Optimism

The S&P 500's performance has been significantly influenced by gains in the technology and AI sectors. Investors are betting on the transformative potential of AI, propelling stocks like Microsoft and Meta to the forefront. However, regulatory scrutiny, such as the FTC's probe into Microsoft's AI software sales, introduces a layer of uncertainty.

Resilient Labor Market

While the Challenger Layoffs report showed a slight uptick, JOLTS job openings rose to 7.744 million in October, indicating a stable labor market. This balance supports the Federal Reserve’s cautious approach to monetary policy, as Chair Jerome Powell reiterated the economy’s strength and gradual progress in reducing inflation.

Mixed Economic Indicators

- **ISM Services PMI** fell to 52.1, below expectations of 55.7, suggesting a slowdown in service sector growth.

- **Durable goods orders** increased by 0.3%, meeting expectations and reinforcing the narrative of economic stability.

- **Construction spending** rose 0.4%, signaling robust investment activity.

- **University of Michigan 1-Year Inflation Prelim** came in at 2.9% (forecast: 2.7%, previous: 2.6%), showing slightly higher inflation expectations.

- **University of Michigan Sentiment Prelim** reached 74 (forecast: 73.2, previous: 71.8), reflecting improved consumer confidence.

These data points reflect a U.S. economy navigating challenges while avoiding a hard landing—a scenario that fuels investor confidence.

---

Federal Reserve Policy: A Turning Point?

Fed officials, including John Williams and Christopher Waller, have hinted at the potential for a December rate cut, with futures markets now pricing in an **85% likelihood of a 25-basis-point reduction**, up from **67%** before the recent jobs report. Inflation progress appears to have stalled, with Fed Governor Michelle Bowman cautioning that more robust measures may be necessary to meet the 2% target by 2025.

The November jobs report further influenced expectations:

- US Nonfarm Payrolls rose to 227k (forecast: 220k, previous: 12k, revised to 36k).

- US Unemployment Rate ticked up to 4.2% (forecast: 4.1%, previous: 4.1%).

- US Average Earnings YoY remained steady at 4% (forecast: 3.9%, previous: 4.0%).

These figures reflect a labor market resilient enough to accommodate rate cuts, which could provide an additional boost to equity markets.

---

Corporate Highlights

- Salesforce reported Q3 revenue of $9.44 billion, exceeding estimates, but missed on adjusted EPS, reflecting mixed investor sentiment.

- Meta (Facebook) is aligning its strategies with evolving political landscapes, as CEO Mark Zuckerberg seeks to navigate regulatory and policy shifts.

- *Microsoft faces FTC scrutiny, underscoring increasing regulatory challenges in the tech sector.

Despite these challenges, corporate earnings have largely supported market valuations, adding another layer of support for the S&P 500.

---

Seasonality and Sentiment

December has historically been a strong month for the S&P 500, driven by:

- Holiday-driven consumer spending.

- Portfolio rebalancing.

- End-of-year tax considerations.

The Fear & Greed Index, currently at 54, indicates a greed-driven sentiment. This optimism aligns with traders pricing in a higher likelihood of Fed rate cuts, reflecting a favorable market environment.

---

Outlook: Optimism with Caution

The S&P 500’s upward momentum is underpinned by strong tech-sector performance, resilient economic data, and seasonal tailwinds. However, challenges such as geopolitical risks, regulatory scrutiny, and uneven progress in disinflation could temper gains.

The Fed's flexibility and potential rate cuts are positive signals for the market, bolstering growth-oriented sectors. Nonetheless, investors should remain vigilant, monitoring corporate earnings, economic releases, and geopolitical developments.

In the near term, the S&P 500 appears poised to end the year on a strong note. However, with inflationary pressures, mixed economic indicators, and geopolitical uncertainties still in play, the path forward will require a delicate balance between economic stability and investor confidence.

SP500 / Key Levels to Watch Amid Jobs DataS&P 500 Technical Analysis

The price dropped from its ATH located at 6099, and still running to get 6058, then should break that by closing 4h or 1h candle below it, to be a more bearish trend toward 6022 and 5972.

The bullish scenario will be solid if can break 6100.

Key Levels:

Pivot Point: 6076

Resistance Levels: 6100, 6143, 6185

Support Levels: 6058, 6022, 5971

ES Levels 12/5 going into NFP FridayGoing to sit out of the release and see how Price Action plays out.

I am expecting lower before the move higher (even if it is just a wick from the release)

Raytehon (RTX) Head and Shoulders. Fundamental reasoning: DJT is a peace president vs Biden who allowed build of geopolitical tensions and warfare.

D.O.G.E dept. to radically overhaul the deep state and waste.

Other notable Military contractors include:.

#LMT

Northrup Grumman

Avic

Boeing

General Dynamics

BAE

ES All Time High Breakout And Targets 12/4Similar to NQ, ES has surged past its previous all-time highs, with a new target of 6,183.75. Since ES has already pulled back to retest the previous highs, it has the potential to continue its rally straight toward the target, but may run into some resistance at the 6,100 level. Stay alert for that ATH price action! 📈 #ES #S&P500 #AllTimeHighs #StockMarket

2024-12-04 - priceactiontds - daily update - sp500Good Evening and I hope you are well.

tl;dr

sp500 e-mini futures - Parabolic buy climax which will end soon. Longs after pullbacks are ok but I will only look for weakness. This is climactic and unsustainable.

comment: Strongest bull bars that late in the trend? Tough. I have two higher targets still. First is the bull trend line to around 6160 and second is a measured move target to 6300. Bears are doing nothing but it’s also unlikely that we just continue higher in this tight of a channel on the daily chart. Market is on it’s last legs up and these windfall profits will get taken off the table before they disappear. You don’t get bullish this late in a trend, you get cautious.

current market cycle: bull trend - late and will end soon

key levels: 6000 - 6170

bull case: Bulls are in complete control but it’s overbought and climactic. the 4h 20ema has been bought for two weeks now and longs near it make sense. Buying above 6050 does not

Invalidation is below 6000.

bear case: Market is overbought and we will likely test down to the 4h 20ema soon. We can’t expect it to just trade through it and we would likely see another bounce up. Bears have nothing until then. Wait for the clear sign that bigger profit taking has started and we do not make new ath every 15m. Slight chance 6102 was the high and we go down to 6000 tomorrow.

Invalidation is above 6170.

short term: Bullish until proven otherwise but will happen sooner than later.

medium-long term - Update from 2024-11-16: So the top definitely qualifies as a blow-off top but the question if we continue further up, is still valid. It is possible that we are already inside the correction and if we continue below 5860, I highly doubt bulls can get above 6000 again. Given the current market structure, I won’t turn bear because the risk of another retest of the highs or even higher ones are just too big.

current swing trade: Nope

trade of the day: Could have bought pretty much anywhere. Again.

Bulls and Bears zone for 12-04-2024It seems that Bulls keep buying and there is no end to this rally.

However, all good things come to an end, it is just matter of time.

Level to watch: 6084 --- 6082

Reports to watch:

US Factory Orders 10:00 AM

US Jerome Powell Speaks 1:40 PM

US Beige Book 2:00 PM

S&P 500 Analysis: Bullish Momentum and Key Levels S&P 500 Technical Analysis

The S&P 500 reached another All-Time High (ATH) in December, signaling a continuation of its bullish trend and the potential for further historical gains.

Currently, the price is consolidating within the range of 6068 and 6022, awaiting a breakout. Overall, the bullish trend remains strong, with the next key target at 6143. However, a break below 6022 could signal a correction, with the price potentially dropping toward 5971.

Key Levels:

Pivot Point: 6068

Resistance Levels: 6100, 6143, 6185

Support Levels: 6022, 5971, 5932

Trend Outlook

The overall trend remains bullish, supported by strong momentum and the recent achievement of new highs.

S&P500: No corrections possibly for the whole 2025.S&P500 is on excellent bullish levels on the 1D timeframe (RSI = 64.149, MACD = 44.390, ADX = 33.789) as it is extending the strong rise since the U.S. elections. Going back even more, this uptrend has been nothing but sustainable ever since the August 5th bottom that almost hit the 1W MA50. In fact that MA level is intact since October 2023. The index has been following a similar path with the December 2018 - December 2021 Bull Cycle that topped after a +105% rise. You can see that following the COVID correction recovery after leg (6), the index crossed over the 1W MA50 and never broke it up until after the January 2022 High in 574 days.

Consequently, we expect a continuation of the current uptrend for as long as the 1W MA50 stays intact. We are targeting a +105% rise yet again (TP = 7,150) near the end of 2025.

See how our prior idea has worked out:

## If you like our free content follow our profile to get more daily ideas. ##

## Comments and likes are greatly appreciated. ##

Are we waiting for #FOMO in #SPX to spark Fomo in #BITCOINSeems, clear to me the obvious answer is YES!

So let's cheer on #STONKS cracking 5,000 on the #S&P

As we would likely see risk be fully turned on, and cash to flow into the #Crypto space.

FWIW

I think the #Economy stinks

but that doesn't necessarily mean assets can't go up in number.

There are plenty of examples where this is the case.

Argentina. Turkey and so on.

#BLOWOFFTOP scenario is still in play.

S&P 500 – Solid Foundation Amid Positive Economic DataS&P 500 – Solid Foundation Amid Positive Economic Data

The S&P 500 index continues to find support from favorable economic data and a stable macroeconomic outlook for the United States. Despite ongoing challenges, the market reflects optimism fueled by a mix of improving manufacturing indicators, resilient consumer spending, and a potential softening in Federal Reserve policy. Additionally, seasonal trends strongly favor the S&P 500, as December is historically one of the best months for equities.

---

Key Economic Drivers Supporting the S&P 500

1. ISM Manufacturing PMI – Signs of Stabilization

- The **ISM Manufacturing PMI** for November rose to 48.4, beating expectations, although still indicating contraction. This suggests the U.S. manufacturing sector is moving closer to stabilization.

- Input costs showed the slowest inflation in a year, and renewed job creation added to the optimism. Challenges such as weaker international demand and reduced production remain, but improved business confidence is a positive signal.

2. Construction Spending Growth

- Construction spending increased by 0.4% in October, highlighting resilience in the housing and infrastructure sectors. This reflects ongoing consumer and government investment, contributing to economic stability.

3. ISM Manufacturing Prices Paid – Easing Inflationary Pressures

- The ISM Manufacturing Prices Paid index dropped to 50.3, well below forecasts of 55.2. This is a significant development for inflation control, signaling moderating cost pressures within the manufacturing sector.

- Implications:

- Positive for equities: Lower inflation reduces the risk of aggressive Federal Reserve rate hikes.

- Stable monetary outlook: This supports expectations of a gradual shift toward easing monetary policy.

4. Fed Officials’ Support for Gradual Easing

- Recent comments from Fed officials indicate a balanced approach toward monetary policy:

- Christopher Waller highlighted the likelihood of a rate cut in December, citing a balanced labor market and gradual progress on inflation.

- John Williams reaffirmed that inflation is expected to decline toward the 2% target while projecting GDP growth of 2.5% in 2024.

- A potential rate cut could provide a further boost to equities as borrowing costs decrease, encouraging corporate investment.

5. Consumer and Business Optimism

- The S&P Global U.S. Manufacturing PMI pointed to renewed job creation and improving confidence, though challenges such as weaker international demand persist. This mix of cautious optimism and moderating inflation supports steady market sentiment.

---

Seasonality and Market Sentiment

Seasonality is a key supporting factor for the S&P 500 at this time. December has historically been a strong month for equity markets due to holiday-driven consumer spending, portfolio rebalancing, and end-of-year tax considerations. This seasonal strength aligns with the Fear & Greed Index, which currently stands at 64, indicating a **greed-driven sentiment** that tends to favor further market upside.

---

S&P 500 Outlook

The S&P 500 is well-positioned to benefit from these positive economic indicators:

- Lower inflationary pressures reduce the likelihood of aggressive Federal Reserve action, which is supportive of equity markets.

- Steady GDP growth and a resilient labor market provide a strong foundation for corporate earnings.

- Improved manufacturing confidence and spending on infrastructure create additional momentum for sectors like industrials and materials.

- Strong seasonality and a favorable market sentiment further reinforce the potential for continued gains.

While global uncertainties and weaker international demand could weigh on certain sectors, the overall outlook for the S&P 500 remains bullish, with near-term support from seasonal trends, improving economic data, and the potential for a more accommodative Fed policy stance.

Elliott Wave View S&P 500 (SPX) Wave 5 in ProgressShort Term Elliott Wave view on SP500 (SPX) suggests rally from 8.5.2024 low is in progress as a 5 waves impulse. Up from 8.5.2024 low, wave 1 ended at 5627.56 high and pullback in wave 2 ended at 5402.62 low. The Index then extends higher in wave 3 ending at 5878.46 high. The next pullback built a zigzag Elliott Wave structure to finish wave 4 at 5696.51 low like the 1 hour chart below shows. Actually, the SPX is trading higher in wave 5 developing an impulse or ending diagonal structure.

Wave 5 rally is in progress with internal subdivision as another impulse. Up from wave 4, wave ((i)) ended at 6017.31 high and wave ((ii)) retracement ended at 5853.01 low. Wave ((iii)) has started and it is trading in wave v of (iii) of ((iii)). Up from wave ((ii)), wave (i) ended at 5908.12 and wave (ii) correction ended at 5855.29. Then the SPX built a nest ending wave i at 5923.51 and wave ii at 5860.56. Wave iii of (iii) finished at 6025.42 and wave iv pullback at 5984.87 low. From here, we are expecting that wave v of (iii) completes soon and the index should see a pullback in 3 swings as wave (iv) before resuming higher in wave (v) of ((iii)). Near term, as far as pivot at 5850.8 low stays intact, expect pullback to find support in 3, 7, or 11 swing for more upside

S&P 500 is climbing upwardsS&P 500 is climbing upwards

The market’s move reflects ongoing digestion of mixed US economic data, supportive seasonality, and cautious optimism among investors.

US Economic Data Highlights

Data provided a mixed snapshot of the US economy, contributing to the market’s recent fluctuations:

- **Chicago Fed National Activity Index (Oct):** Fell to -0.40, below the expected -0.2.

- **Dallas Fed Manufacturing Index (Nov):** Came in at -2.7, worse than the forecast of -2.4.

- **New Home Sales (Oct):** Declined to 0.61M, significantly missing expectations of 0.73M.

- **Richmond Fed Manufacturing Index (Nov):** Plunged to -14, below the forecast of -10.

- **Durable Goods Orders (Oct):** Increased by just 0.2%, underperforming the 0.5% forecast.

- **Initial Jobless Claims (Nov 23):** Reported at 213K, slightly better than expected (216K), but still pointing to a resilient labor market.

- **Chicago PMI (Nov):** Dropped to 40.2, well below the anticipated 44, highlighting weakness in manufacturing.

Market Sentiment and Seasonality

Seasonality continues to work in favor of the S&P 500, as historical trends during this period often support equities. The **Fear & Greed Index**, currently at **66 points**, reflects moderate optimism and a "Greed" sentiment, which typically aligns with risk-on behavior in the markets.

Rate Cut Expectations

Markets remain focused on the Federal Reserve’s upcoming meeting on **December 18th**, with a **62,2%% probability** currently priced in for a **25 basis-point rate cut**. Such a move could provide additional support for equities by easing financial conditions, though its long-term impact remains uncertain.

Geopolitical Risks

While market sentiment has improved slightly, risks remain in the background. The ongoing war in Ukraine continues to pose threats to global stability, with potential knock-on effects on energy prices, supply chains, and economic performance.

Long-Term Trend Intact, but Volatility Likely

The S&P 500’s long-term upward trend remains intact, bolstered by supportive seasonality, stable GDP growth, and investor optimism. However, the current environment of mixed economic data and rising policy uncertainty suggests that market volatility could persist in the short term.

Broader Context

27.11 data underscored a steady but moderating US economy, while forward-looking risks remain:

- **Global Economic Outlook:** The S&P Global forecast anticipates global GDP growth of approximately 3% by 2025, with US growth slowing to below 2% next year and China toward 4%.

- **US Policy Risks:** Potential policy shifts under the new administration could elevate inflation pressures and tighten financial conditions, introducing further uncertainty for equity markets.

Implications for S&P 500

Today’s modest gain shows resilience in the face of mixed signals from economic data and global risks. With supportive seasonality and a strong likelihood of a December rate cut, the S&P 500 may find short-term support. However, investors should remain vigilant, as volatility is likely to persist amid policy uncertainties and geopolitical risks.

What’s your outlook for the S&P 500 after today’s rebound? Can the market sustain its gains, or will headwinds from mixed data and global risks take over? Share your thoughts in the comments!

The EUR/USD forecast for reaching 1.11 by December 2024The EUR/USD forecast for reaching 1.11 by December 2024 might seem ambitious given current trends, but let's delve into why this could indeed happen:

Economic Recovery in the EU: Recent posts on X highlight expectations around the ECB's monetary policy. If the European Central Bank continues to adjust rates in response to economic recovery signals, a stronger Euro might follow. Discussions around inflation cooling off and potential rate adjustments suggest a more robust Eurozone economy, which traditionally supports a higher EUR/USD rate.

Political Stability and Sentiment: With the U.S. political landscape shifting due to the Democratic nomination of Kamala Harris for the 2024 election, there's a narrative shift. While not directly economic, political stability or perceived changes in policy direction can influence currency strength. If her campaign promises economic policies that might strengthen the Euro against the Dollar, this could be a psychological boost for EUR/USD.

Market Sentiment and Speculation: There's noticeable chatter on platforms like X about EUR/USD movements. Speculation can drive markets; if traders and investors start betting on a stronger Euro due to any positive economic data or geopolitical shifts, this speculative buying could push the rate towards 1.11.

Technical Analysis: Some analysts have pointed out key resistance and support levels. Breaking through these levels, especially with momentum, could set new targets. If EUR/USD manages to convincingly breach the 1.09 resistance and maintain that level, the next psychological target becomes 1.10, with 1.11 not far beyond in terms of market psychology.

Interest Rate Differentials: If the ECB's rate adjustments lead to a narrowing of the interest rate differential with the Fed, capital flow might favor the Euro more, pushing its value up against the Dollar. Given historical trends, even a small change in rate expectations could significantly impact the forex market.

Global Economic Factors: Broader economic conditions, like improvements in European trade balances, could bolster the Euro. If the EU manages to show resilience or growth in sectors previously affected by global downturns, this could reflect positively on the EUR.

Seasonal Trends and Market Calendar: There's often a lull before the end-of-year where markets might move based on year-end portfolio adjustments. If there's a sentiment that the Euro will strengthen, this could be the period where movements towards 1.11 get traction due to year-end positioning.

S&P: Weekly Recap and OutlookLast week, the market opened with a gap up that was quickly filled, after which price hovered near the previous all-time high. Bolstered by new economic data, which delivered no negative surprises, bulls pushed the price out of the trading range, establishing a new all-time high.

While this is undoubtedly a positive development that reinforces the bullish thesis, a few warning signs warrant closer attention:

1. Low Breakout Volume: The breakout occurred on significantly low volume. While volume is less critical in indices and ETFs compared to individual stocks, observing below-average volume during such an important event raises concerns about the breakout’s sustainability.

2. Relative Weakness in the Tech Sector (XLK): This deviation signals hesitancy among growth investors, which could potentially ripple through to other market participants.

Additionally, concerns highlighted in my previous review remain unresolved and continue to be relevant.

At this stage, there is no concrete evidence of a sentiment shift or technical signals pointing to a broad trend reversal. However, there is a growing impression that the rally may be nearing temporary exhaustion, which could lead to a significant pullback.

Key Focus for the Upcoming Week

Investors will be closely watching the employment data, which has already hinted at labor market weakness. If new data further support this trend, it could heighten bearish sentiment.

Price action this week will likely provide important clues:

• Bullish Confirmation: If the breakout is followed by a swift continuation, this will confirm buyers’ conviction and overall market strength.

• Bearish Signals: Conversely, if the price pulls back below 600 or oscillates indecisively around this level, it may signal uncertainty among buyers, creating an opportunity for short sellers to capitalize.

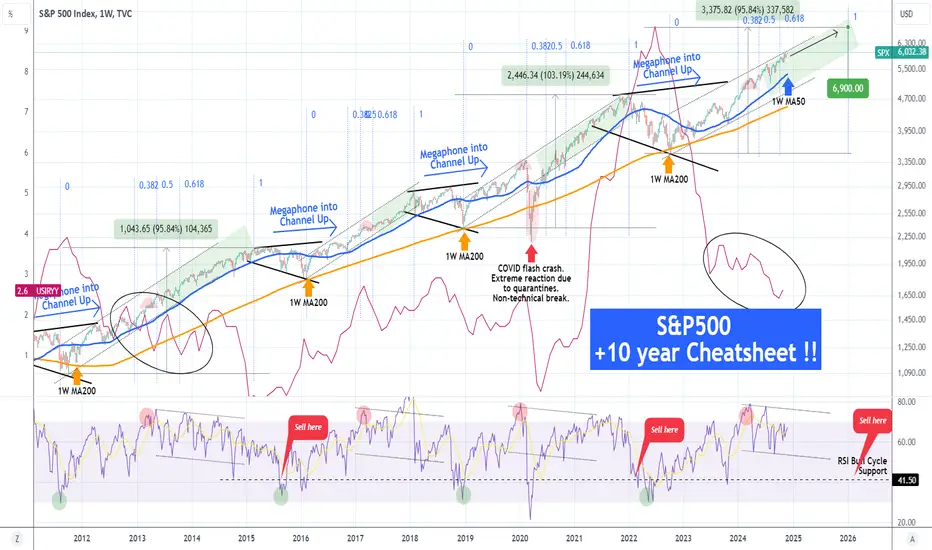

S&P500 This Inflation Cheatsheet shows no correction in 2025.This is a chart we first posted almost 4 months ago (August 14, see chart below) at the time of a CPI date release, where we viewed the S&P500 index (SPX) against Inflation (red trend-line) and calling for an immediate buy:

** The 1W MA50 as the ultimate Support **

Well the price jumped +11% since then from 5440 to over 6000. The first principle of this chart is that as long as the 1W MA50 (blue trend-line) is supporting, investors should stay bullish. This is because all previous multi-year rallies since August 2011 that started within a Channel Up, ended upon a 1W candle close below the 1W MA50 and transitioned into a Megaphone pattern for the new Bear Phase.

** Declining Inflation fueling stocks **

Right now we are still on a declining Inflation trend, very similar to early 2014 (ellipse shape on Inflation), while the 1W RSI of SPX is declining inside a Channel Down. This is a Bearish Divergence, which during all previous SPX Channel Up patterns, didn't make the index top until the RSI broke below its 41.50 Support (notable exception of course the March 2020 COVID flash crash which was a one in 100 years Black Swan event).

** SPX Target and timing **

As a result, while the 1W RSI trades within its Channel Down and above 41.50 and all price candles close above the 1W MA50, we expect the index to extend the multi-year uptrend to 6900, which would represent a +95.84% rise from the October 2022 bottom, similar to the February 2015 High. Notice that the December 2021 top was also of a similar magnitude (+103%).

As far as timing is concerned, we have calculated a model based on the 1W RSI top and the start of its Channel Down. As you see at that point, SPX always makes a medium-term pull-back (red Arc). This tends to be within the 0.382 - 0.618 time Fibonacci levels and on the 2011 - 2014 Bull Cycle, that was within the 0.382 - 0.5 Fib zone. As a result, applying this principle on the current Bull Cycle, the trend is now just 2 months past the 0.618 time Fib and we can expect a Cycle Top around December 2025.

-------------------------------------------------------------------------------

** Please LIKE 👍, FOLLOW ✅, SHARE 🙌 and COMMENT ✍ if you enjoy this idea! Also share your ideas and charts in the comments section below! This is best way to keep it relevant, support us, keep the content here free and allow the idea to reach as many people as possible. **

-------------------------------------------------------------------------------

💸💸💸💸💸💸

👇 👇 👇 👇 👇 👇

SPX: positive sentiment will holdAnalysts are noting that the S&P 500 ended its best week in 2024. Although the year is slowly approaching the New Year holidays in December, the market sentiment continues to remain quite strong. The index reached its fresh new all time highest level at 6.043, breaking its 6K level.

One of the topics which pushed the semiconductor and chip producers shares to the upside was the Bloomberg report, which noted that additional barriers on the sale of semiconductors to China, imposed by the Biden administration, was not so severe, as the market previously perceived. Market favourite Nvidia surged by 3%, while other semiconductor and chip producers followed the move. Some influence to the equity market came also from the US bonds market, which eased in expectation of further rate cuts and its positive impact to the economy.

As per CME Group FedWatch Tool there is currently 66% odds that the Fed will cut interest rates at their December meeting by additional 25 bps. As long as such a sentiment strongly holds on the market, it could be expected to have a further positive impact on the value of the equity index till its final slowdown nearing the New Year Holiday. At this point, the S&P 500 gained around 24% for the year, which is its best yearly results since 2021.

#202448 - priceactiontds - weekly update - sp500 e-mini futurestl;dr

sp500 e-mini futures: Max bullish. New ath is done, now I have two upper targets left for this year. We have 2 decent upper bull trend lines where only the #1 target of 6300 fits. The other would be 6450 but too far and too low probability for now. Bears would need anything below 5850 to kill the rally.

Quote from last week:

comment: Bullish bias I had, bullish it was. Market looks like it wants up bad. Every dip is bought heavily on increasing volume. Time is now to get above 6100 or we won’t get it at all. Market is beyond overvalued, overbought and the poor late bulls are just arriving. Guess who will be left holding the bags again.

comment: Bullish bias I had, bullish it was. Again. Market wanted up and it got it. Is this stopping here? Probably not. Look for longs .

current market cycle: Bull trend

key levels: 5850 - 6150 (maybe even 6500)

bull case: Last hurrah. 6150 is my next target and if we don’t stop, 6500. Is this a bubble? Yes. Can you short this? No. Trends can go much further than anyone can imagine and your account can not sustain the drawdown of early shorts. Breakout is clear, as is the chart.

Invalidation is below 5850.

bear case: Non-starter is this here. Daily close below 5850, then I start looking at this with a bigger bullish eye.

Invalidation is above 6070.

outlook last week:

short term: I want to join the bulls again. Need strong confirmation first though. Still no interest in selling as of now.

→ Last Sunday we traded 5987 and now we are at 6051. Perfect outlook.

short term: Bullish all the way. If market closes below 5900 I would turn neutral and daily close below 5800 would probably be the end of my bullish thesis and I turn bear.

medium-long term - Update from 2024-11-24: 6150 and 6500 are my last targets for the bulls before this bubble begins to pop or at least deflate.

current swing trade: None

chart update: Nothing.

S&P 500 is climbing upwardsS&P 500 is climbing upwards

The market’s move reflects ongoing digestion of mixed US economic data, supportive seasonality, and cautious optimism among investors.

US Economic Data Highlights

Data provided a mixed snapshot of the US economy, contributing to the market’s recent fluctuations:

- **Chicago Fed National Activity Index (Oct):** Fell to -0.40, below the expected -0.2.

- **Dallas Fed Manufacturing Index (Nov):** Came in at -2.7, worse than the forecast of -2.4.

- **New Home Sales (Oct):** Declined to 0.61M, significantly missing expectations of 0.73M.

- **Richmond Fed Manufacturing Index (Nov):** Plunged to -14, below the forecast of -10.

- **Durable Goods Orders (Oct):** Increased by just 0.2%, underperforming the 0.5% forecast.

- **Initial Jobless Claims (Nov 23):** Reported at 213K, slightly better than expected (216K), but still pointing to a resilient labor market.

- **Chicago PMI (Nov):** Dropped to 40.2, well below the anticipated 44, highlighting weakness in manufacturing.

Market Sentiment and Seasonality

Seasonality continues to work in favor of the S&P 500, as historical trends during this period often support equities. The **Fear & Greed Index**, currently at **64 points**, reflects moderate optimism and a "Greed" sentiment, which typically aligns with risk-on behavior in the markets.

Rate Cut Expectations

Markets remain focused on the Federal Reserve’s upcoming meeting on **December 18th**, with a **66,3%% probability** currently priced in for a **25 basis-point rate cut**. Such a move could provide additional support for equities by easing financial conditions, though its long-term impact remains uncertain.

Geopolitical Risks

While market sentiment has improved slightly, risks remain in the background. The ongoing war in Ukraine continues to pose threats to global stability, with potential knock-on effects on energy prices, supply chains, and economic performance.

Long-Term Trend Intact, but Volatility Likely

The S&P 500’s long-term upward trend remains intact, bolstered by supportive seasonality, stable GDP growth, and investor optimism. However, the current environment of mixed economic data and rising policy uncertainty suggests that market volatility could persist in the short term.

Broader Context

27.11 data underscored a steady but moderating US economy, while forward-looking risks remain:

- **Global Economic Outlook:** The S&P Global forecast anticipates global GDP growth of approximately 3% by 2025, with US growth slowing to below 2% next year and China toward 4%.

- **US Policy Risks:** Potential policy shifts under the new administration could elevate inflation pressures and tighten financial conditions, introducing further uncertainty for equity markets.

Implications for S&P 500

Today’s modest gain shows resilience in the face of mixed signals from economic data and global risks. With supportive seasonality and a strong likelihood of a December rate cut, the S&P 500 may find short-term support. However, investors should remain vigilant, as volatility is likely to persist amid policy uncertainties and geopolitical risks.

What’s your outlook for the S&P 500 after today’s rebound? Can the market sustain its gains, or will headwinds from mixed data and global risks take over? Share your thoughts in the comments!

S&P 500 HYPERWAVE CRASH The S&P 500 is currently going through a huge macro hyper-wave, this has been confirmed. This has already been calculated and factored into the 'algo', I'm highly confident we are approaching the final stages of 'wave 4' which will end in resumption to the downside (wave 5) and followed by the 'bounce' or 'wave 6'. After wave 6 has concluded, it's game over. Wave 7 will complete the hyper-wave and will be catastrophic to not only the markets but the economy by extension... please keep this in mind as when this all comes down we're entering something far worse than the 1929 crash and the great depression that followed.