GBPKPYHey Traders, we are monitoring GBPJPY for a buying opportunity around 153 zone at the retrace, once we will receive any bullish confirmation the trade will be executed.

Trade Safe, Joe.

Poundsterling

GBPNZDHey Traders, we are monitoring GBPNZD for a buying opportunity around 1.911 zone, once we will receive any bullish confirmation the trade will be executed.

Trade Safe and use proper risk management.

Today’s Notable Sentiment ShiftsUSD – The dollar rose slightly as the US Federal Reserve prepared on Tuesday to kick off its two-day policy meeting where it was expected to announce the start of tapering of its massive asset purchases put in place at the start of the COVID-19 pandemic.

GBP – The pound edged lower on Tuesday, hovering around a three-week low, pressured by uncertainty about whether the Bank of England will raise interest this week.

Commenting on GBP, CIBC stated that “sterling looks set to remain on the defensive. Ahead of UK final services PMI tomorrow and the BoE decision on Thursday, analysts remain split between no change and a 15bp hike. We narrowly favour the former.”

AUD – The Aussie dollar weakened across the board following the RBA’s overall dovish November policy meeting. Despite the central bank dropping its commitment to keep bond yields low.

NAB noted that:

“The RBA has made every effort to sound dovish. There’s nothing in the statement to endorse market prcing that has the RBA moving in 2022, so in that sense there’s clearly an attempt to push back on market pricing.

Their forecasts, which we get on Friday, could be consistent with a move in 2023, but certainty not in 2022.

In the last week or so there’s been a tug of war between the big falls we’ve seen in commodity prices and the big moves we’ve seen in Aussie interest rates, particularly real interest rates. Arguably now, that tug of war for the moment is being resolved with both lower rates and falling commodity prices, so on that basis I would say that the risk is that we could see some further slippage in the Aussie dollar near term.”

Today’s Notable Sentiment ShiftsGBP – The pound slipped on Monday, touching its lowest in more than two weeks versus the dollar and euro, pressured by uncertainty over the Bank of England’s policy stance and an escalating post-Brexit spat with France over fish.

BMO Capital Markets added that “FX investors have become more concerned about the inflation backdrop in the context of hawkish shifts by numerous central banks. This has, in turn, reduced risk appetite levels and the extent of upward pressure on sterling/dollar. BoE hawkishness is unlikely to translate directly into pound appreciation versus the dollar in the current environment.”

GBP JPY - FUNDAMENTAL DRIVERSGBP

FUNDAMENTAL BIAS: BULLISH

1. The Monetary Policy outlook for the BOE

The Sep policy meeting from the BoE saw money markets rushing to price in a much faster and more aggressive policy path than previously expected. Even though this of course falls in line with our bullish bias for the Pound, we do think the market is a bit too aggressive too quick right now. The bank did explain that they now see inflation above 4% by Q4 of this year, and the possibility of more sticky inflation was the key reasons why we saw a 7-2 QE vote split with Saunders and Ramsden both dissenting to cut purchases. However, it’s important to note that the remaining 7 members still see inflation as transitory, and the fact that they expect CPI above 4% means any prints that don’t come close to that poses downside risks. Furthermore, even though the bank said their expectations of modest tightening has strengthened, the admitted that lots of uncertainties remain. A big one of these is the labour market, where even though the number of furloughed staff have decreased, that decrease has materially slowed from August which poses more uncertainty for the labour market. Thus, even though our bias remains unchanged, and we see the bank lifting rates in Q4, we do think the over optimistic moves in money markets poses short-term headwinds. Make sure to catch this week’s Top Trading Opportunity Report and Week Ahead Video in the terminal for more info on the event.

2. The country’s economic developments

The successful vaccination program that allowed the UK to open faster and sooner than peers provided a favourable environment for Sterling and the strength of the economic recovery has meant solid growth differentials favouring GBP. However, a lot of these positives are arguably priced, and the recent slowdown in activity data that suggests peak growth has been reached and could mean an uphill push for GBP to see the same outperformance we saw earlier. With our above comments about money markets, it also means that there is now more risk to downside surprises than was the case a few months ago.

3. Political Developments

Even though a Brexit deal was reached last year, some issues like the Northern Ireland protocol remains, and with neither side willing to budge it seems like these issues. Two weeks ago, the EU ramped up some political posturing with reports that said they are mulling terminating the Brexit deal if the UK triggers Article 16. For now, these are just threats, but with rates markets still very aggressively priced any further escalation could increase the odds of seeing repricing downside in the GBP, so one to keep on the radar alongside the fishing row with France.

4. CFTC Analysis

Latest CFTC data showed a positioning change of +13338 with a net non-commercial position of +14953. Sterling have seen a very impressive rebound from recent lows as markets reacted positively to recent BoE comments which sparked additional downside in SONIA futures and expectations of higher rates. Right now, money markets are pricing in a 15-basis point hike in Q4 and four additional 25-basis point hikes by end 2022. Even though GBP has enjoyed a bounce back in positioning, Sterling has been mostly rangebound since the start of September as traders arguably want to keep their powder dry for this week’s very important BoE policy decision. Positioning is not in stress territory for large specs or leveraged funds which means positioning shouldn’t affect either hawkish or dovish tilts from the BoE this week.

JPY

FUNDAMENTAL BIAS: BEARISH

1. Safe-haven status and overall risk outlook

As a safe-haven currency, the market's risk outlook is the primary driver of JPY. Economic data rarely proves market moving; and although monetary policy expectations can prove highly market-moving in the short-term, safe-haven flows are typically the more dominant factor. The market's overall risk tone has improved considerably following the pandemic with good news about successful vaccinations, and ongoing monetary and fiscal policy support paved the way for markets to expect a robust global economic recovery. Of course, there remains many uncertainties and many countries are continuing to fight virus waves, but as a whole the outlook has kept on improving over the past couple of months, which would expect safe-haven demand to diminish and result in a bearish outlook for the JPY.

2. Low-yielding currency with inverse correlation to US10Y

As a low yielding currency, the JPY usually shares an inverse correlation to strong moves in yield differentials, more specifically in strong moves in US10Y . However, like most correlations, the strength of the inverse correlation between the JPY and US10Y is not perfect and will ebb and flow depending on the type of market environment from a risk and cycle point of view. With bond yields looking a bit stretched at the current levels any decent mean reversion is expected to be supportive for the JPY, so it remains a key asset class to keep track.

3. CFTC Analysis

Latest CFTC data showed a positioning change of -4302 with a net non-commercial position of -107036. The past few weeks of price action in the JPY was mostly driven by the excessive moves we saw in yields on the US side but was also exacerbated by risk on flows and rising oil prices which is a negative driver for Japan for its terms of trade. Even though the bias for the JPY remains firmly tilted to the downside, the moves across JPY pairs is arguably still looking stretched, and with both large speculators and leveraged funds firmly in net-short territory the odds of some mean reversion has increased. We would prefer waiting for some of the froth to mean revert before looking for new JPY shorts. As always, any major risk off flows can still support the JPY, especially with quite a sizable net-short position still built up in the currency for large speculators as well as leveraged funds, but rates have been the key driver in the short-term.

GBP/USD - Buying opportunity, close to oversold areas😋Technical Overview: - GBP/USD

Analysis is only 1 piece of the puzzle 🧩

Our analysis is a sentiment for the upcoming week, month.

Use this as a weather forecast, you are the person that has to put on a jacket when it’s raining.

Trade this sentiment based off your own entry strategy at the right time.

Flow with the Devil 😈

Trade with the manipulation👾

GBPUSD 1 MONTH LEFT OF DROPHello , its been 4 months since pound was dropping reaching 2 level of drop , for now im expecting another and last level of drop since its 31/OCT/2020 to make the cycle complet.

you can sell on H4 order block.

GBPUSD - 30 min - Change of Bias - Further upside comingGbpusd - 30 mins - Yesterdays bearish bias has been changed into a bullish one after yesterdays price action on dollar pairs. I see further upside coming for gbpusd upto 1.39 before a major bearish reversal.

LONG ENTRY on GBPUSDLONG ENTRY on GBPUSD with the following stats:

Entry @1.37959

Target 1 @1.38951

Target 2 @1.40564

Trailing Stop @1.35260

Will pull in stop to trail from break even if/when Target 1 is hit.

EUR GBP BUY - (EURO - POUND STERLING)Hi there.

Price is moving impulsively to the upside.

Wait for the price to form a consolidation on lower time frame and watch strong price action for buy.

GBPUSD SELLWelcome, traders.

By "following", you can always get new information quickly.

Please also click "Like".

Have a nice day.

GBPJPY : Possibility of having a bearish coontinuation.Well a possibile touch of 156.820 and price creating a strong selling pressure might trigers my mind in going bearish on gbpjpy....

GBPUSD Entry - Continued Bull Market 1.37656 NOV 15-17th British Pound started my whole adventure in Fish N Pips. I'm trying to validate which currencies will swing and the impact on the dollar. The technical analysis on the Monthly chart is Bull Trend for $GBPUSD. I consider new entry point in few weeks as the RSI band nears the tipping point in the Gann Fann 8/1

Happy trading!

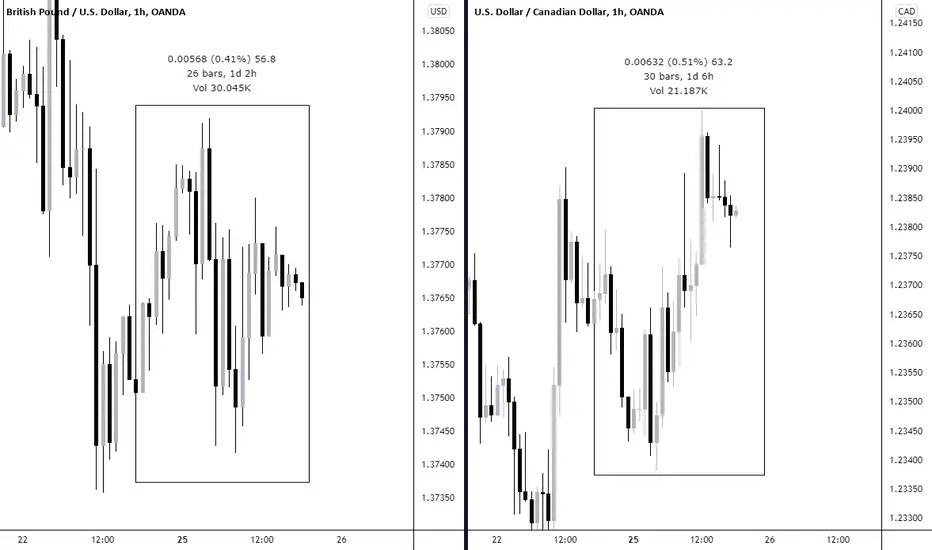

Today’s Notable Sentiment ShiftsGBP – Sterling rose to 20-month highs against the euro on Tuesday, driven by diverging interest rate expectations for Britain and the Eurozone, especially after data showed UK full-time earnings rising by the most since 2008.

However, MUFG warns its investor that “there is an element of caution in chasing the pound higher on the back of higher rates. The combination of slower growth and higher inflation is not a good mix for a currency.”

GBP/USD_4H_LongPrice broke the descending channel and previous weekly high and a weekly resistance, also it is making a pullback in daily, and in 4H it is almost bullish, so a long position taken and the TP is put on that last high that makes the bearish trend near the next monthly resistance.

R/R = 1:2.25

Today’s Notable Sentiment ShiftsGBP – Sterling rose slightly on Monday but remained within recent ranges as analysts said concerns about economic growth and inflation limited its gains from expectations that the Bank of England will raise rates.

Reports from Societe Generale noted that their analysts believe “the FX market is going to blindly buy sterling on rate hikes that are down to supply-side inflationary pressures (Brexit having made sure the UK feels these particularly sharply) against the backdrop of a dismal run of falling monthly retail sales figures.”

CAD – The Canadian dollar weakened against its US counterpart on Monday, as oil gave back its earlier gains, and investors weighed the potential for the Bank of Canada to push against recent moves by the market to price in multiple rate hikes next year.

EUR GBP BUY - (EURO - POUND STERLING)Hi there.

Price is forming a reversal pattern to change its direction.

Watch strong price action at the current levels for buy.

GBP USD - FUNDAMENTAL DRIVERSGBP

FUNDAMENTAL BIAS: BULLISH

1. The Monetary Policy outlook for the BOE

The Sep policy meeting from the BoE saw money markets rushing to price in a much faster and more aggressive policy path than previously expected. Even though this of course falls in line with our bullish bias for the Pound, we do think the market is a bit too aggressive too quick right now. The bank did explain that they now see inflation above 4% by Q4 of this year, and the possibility of more sticky inflation was the key reasons why we saw a 7-2 QE vote split with Saunders and Ramsden both dissenting to cut purchases. However, it’s important to note that the remaining 7 members still see inflation as transitory, and the fact that they expect CPI above 4% means any prints that don’t come close to that poses downside risks. Furthermore, even though the bank said their expectations of modest tightening has strengthened, the admitted that lots of uncertainties remain. A big one of these is the labour market, where even though the number of furloughed staff have decreased, that decrease has materially slowed from August which poses more uncertainty for the labour market. Thus, even though our bias remains unchanged, and we see the bank lifting rates in Q1, we do think the over optimistic moves in money markets poses short-term headwinds.

2. The country’s economic developments

The successful vaccination program that allowed the UK to open faster and sooner than peers provided a favourable environment for Sterling and the strength of the economic recovery has meant solid growth differentials favouring GBP. However, a lot of these positives are arguably priced, and the recent slowdown in activity data that suggests peak growth has been reached and could mean an uphill push for GBP to see the same outperformance we saw earlier. With our above comments about money markets, it also means that there is now more risk to downside surprises than was the case a few months ago.

3. Political Developments

Even though a Brexit deal was reached last year, some issues like the Northern Ireland protocol remains, and with neither side willing to budge it seems like these issues. On Friday, the EU ramped up some political posturing with reports that said they are mulling terminating the Brexit deal if the UK triggers Article 16. For now, these are just threats, but with rates markets still very aggressively priced any further escalation could increase the odds of seeing repricing downside in the GBP, so one to keep on the radar after Friday.

4. CFTC Analysis

Latest CFTC data showed a positioning change of +13594 with a net non-commercial position of +1615. Sterling have seen a very impressive rebound from recent lows as markets reacted positively to recent BoE comments which sparked additional downside in SONIA futures , which are now fully priced for a 15-basis point hike in Q4 and about three 25-basis point hikes by end 2022. Even though GBP has enjoyed upside on the tightening expectations, the reasons why markets are pricing a steeper rate path is out of fear of inflation and not due to a more positive economic outlook, which as we highlighted above does pose headwinds for the Pound in the weeks ahead if growth or inflation data surprise lower in the weeks ahead.

USD

FUNDAMENTAL BIAS: WEAK BULLISH

1. The Monetary Policy outlook for the FED

More hawkish than expected sums up the Sep meeting. The FOMC gave the go ahead for a November tapering announcement as long as the economy develops as expected with their criteria for substantial further progress close to being met. The biggest hawkish tilt was the announcement about a faster pace of tapering, with Chair Powell saying there is broad agreement that tapering can be concluded by mid2022. Inflation projections were hawkish, with the Fed projecting Core PCE above their 2% until 2024. On labour, Chair Powell said he thought the substantial further progress threshold for employment was ‘all but met’ and explained that it won’t take a very strong September jobs print for them to start tapering as just a ‘decent’ print will do. The 2022 Dots stayed very close to the June median, but the rate path was much steeper than markets were anticipating with seven hikes expected over the forecast horizon (from just two previously). It is important here to note though that even though the path was steeper, if one compares that to a projected Core PCE >2% for 2022 to 2024, the rate path does not exactly scream fear when it comes to inflation . All in all, it was a hawkish meeting. Interestingly, it took markets about three days to realize this as the expected price action only really took hold of markets a few days later. A faster tapering was a key factor we were watching for an incrementally bullish tilt in the outlook, so market’s initial reactions were surprising. However, with the recent breakout in both US yields and the USD, this has given us more confidence in moving our fundamental outlook for the Dollar from Neutral to Weak Bullish .

2. Real Yields

With a Q4 taper start and mid-2022 taper conclusion on the card, we think further downside in real yields will be a struggle and the probability are skewed higher given the outlook for growth, inflation and policy, and higher real yields should be supportive for the USD in the med-term .

3. The global risk outlook

One supporting factor for the USD from June was the onset of downside surprises in global growth. However, recent Covid-19 case data from ourworldindata. org has shown a sharp deceleration in new cases globally. Using past occurrences as a template, the reduction in cases is likely to lead to less restrictive measures, which is likely to lead to a strong bounce in economic activity. Thus, even though we have shifted our bias to weak bullish in the med-term , the fall in cases and increased likelihood of a bounce in economic activity could mean downside for the USD from a short to intermediate time horizon (remember a re-acceleration in growth and potentially inflation = reflation)

4. Economic Data

Economic data will be very light in the incoming week with the main highlights being PCE and Advanced GDP (old news). Also keep in mind that the Fed has largely reduced the impact of economic data going into the November FOMC meeting by already acknowledged a Nov taper and a possible mid-2022 conclusion. So, even though data will be important, it’s unlikely to sway the Fed from their tapering plans.

5. CFTC Analysis

Latest CFTC data showed a positioning change of +872 with a net non-commercial position of +35934. Positioning isn’t anywhere near stress levels for the USD, but the speed of the build-up in large specular positioning measures over 2-standard deviation on a 1-year look back period. Thus, even though the med-term bias remains unchanged, it does mean the USD could be sensitive to mean reversion risks while still trading close to YTD highs. Thus, reflationary data and overall risk sentiment will be a key focus for the USD in the week ahead.

GBP JPY - FUNDAMENTAL DRIVERSGBP

FUNDAMENTAL BIAS: BULLISH

1. The Monetary Policy outlook for the BOE

The Sep policy meeting from the BoE saw money markets rushing to price in a much faster and more aggressive policy path than previously expected. Even though this of course falls in line with our bullish bias for the Pound, we do think the market is a bit too aggressive too quick right now. The bank did explain that they now see inflation above 4% by Q4 of this year, and the possibility of more sticky inflation was the key reasons why we saw a 7-2 QE vote split with Saunders and Ramsden both dissenting to cut purchases. However, it’s important to note that the remaining 7 members still see inflation as transitory, and the fact that they expect CPI above 4% means any prints that don’t come close to that poses downside risks. Furthermore, even though the bank said their expectations of modest tightening has strengthened, the admitted that lots of uncertainties remain. A big one of these is the labour market, where even though the number of furloughed staff have decreased, that decrease has materially slowed from August which poses more uncertainty for the labour market. Thus, even though our bias remains unchanged, and we see the bank lifting rates in Q1, we do think the over optimistic moves in money markets poses short-term headwinds.

2. The country’s economic developments

The successful vaccination program that allowed the UK to open faster and sooner than peers provided a favourable environment for Sterling and the strength of the economic recovery has meant solid growth differentials favouring GBP. However, a lot of these positives are arguably priced, and the recent slowdown in activity data that suggests peak growth has been reached and could mean an uphill push for GBP to see the same outperformance we saw earlier. With our above comments about money markets, it also means that there is now more risk to downside surprises than was the case a few months ago.

3. Political Developments

Even though a Brexit deal was reached last year, some issues like the Northern Ireland protocol remains, and with neither side willing to budge it seems like these issues. On Friday, the EU ramped up some political posturing with reports that said they are mulling terminating the Brexit deal if the UK triggers Article 16. For now, these are just threats, but with rates markets still very aggressively priced any further escalation could increase the odds of seeing repricing downside in the GBP, so one to keep on the radar after Friday.

4. CFTC Analysis

Latest CFTC data showed a positioning change of +13594 with a net non-commercial position of +1615. Sterling have seen a very impressive rebound from recent lows as markets reacted positively to recent BoE comments which sparked additional downside in SONIA futures, which are now fully priced for a 15-basis point hike in Q4 and about three 25-basis point hikes by end 2022. Even though GBP has enjoyed upside on the tightening expectations, the reasons why markets are pricing a steeper rate path is out of fear of inflation and not due to a more positive economic outlook, which as we highlighted above does pose headwinds for the Pound in the weeks ahead if growth or inflation data surprise lower in the weeks ahead.

JPY

FUNDAMENTAL BIAS: BEARISH

1. Safe-haven status and overall risk outlook

As a safe-haven currency, the market's risk outlook is the primary driver of JPY. Economic data rarely proves market moving; and although monetary policy expectations can prove highly market-moving in the short-term, safe-haven flows are typically the more dominant factor. The market's overall risk tone has improved considerably following the pandemic with good news about successful vaccinations, and ongoing monetary and fiscal policy support paved the way for markets to expect a robust global economic recovery. Of course, there remains many uncertainties and many countries are continuing to fight virus waves, but as a whole the outlook has kept on improving over the past couple of months, which would expect safe-haven demand to diminish and result in a bearish outlook for the JPY.

2. Low-yielding currency with inverse correlation to US10Y

As a low yielding currency, the JPY usually shares an inverse correlation to strong moves in yield differentials, more specifically in strong moves in US10Y . However, like most correlations, the strength of the inverse correlation between the JPY and US10Y is not perfect and will ebb and flow depending on the type of market environment from a risk and cycle point of view. With bond yields looking a bit stretched at the current levels any decent mean reversion is expected to be supportive for the JPY, so it remains a key asset class to keep track.

3. CFTC Analysis

Latest CFTC data showed a positioning change of -26100 with a net non-commercial position of -102734. The past few days of price action in the JPY was mostly driven by the excessive moves we saw in yields on the US side but was also exacerbated by risk on flows and rising oil prices which is a negative driver for Japan for its terms of trade. Even though the bias for the JPY remains firmly tilted to the downside, the move is looking stretched, and with both large speculators and leveraged funds firmly in net-short territory the odds of some mean reversion has increased, and we would prefer waiting for some of the froth to mean revert before looking for new JPY shorts. As always, any major risk off flows can still support the JPY, especially with quite a sizable net-short position still built up in the currency for large speculators as well as leveraged funds, but rates have been the key driver in the short-term.

GBPNZD: Catching a Pullback 🇬🇧🇳🇿

GBPNZD dropped to a key level.

Analyzing the intraday perspective the reaction to that structure was overwhelmingly bullish:

the price managed to break and close above a resistance line of a falling parallel channel on 4H.

Now the price may go higher.

Next resistance - 1.933

❤️Please, support this idea with like and comment!❤️

GBP JPY SELL - (POUND STERLING - JAPANESE YEN)Hi there.

Pirce is forming a reversal pattern to change its direction.

Watch strong price action at the current levels for sell.

Today’s Notable Sentiment ShiftsUSD – The dollar dipped on Wednesday as risk sentiment improved and as investors focused on rising commodity prices and when global central banks are likely to begin hiking interest rates to fend off persistently high inflation.

GBP – Sterling traded near a one-month high on Wednesday after traders said a dip in September inflation was unlikely to stop the Bank of England from raising interest rates soon.

CAD – The Canadian dollar edged higher as CPI data showed an 18-year high, supporting the market’s “hawkish outlook” for the BoC and offsetting a drop in oil prices.

EURGBP: Potential Trend-Following Setup 🇪🇺🇬🇧

Hey traders,

This morning with my students we discussed a shorting opportunity on EURGBP.

The pair is trading in a downtrend.

Retracing from 0.842 level, the price reached 0.8465 strong resistance cluster.

On that, the pair formed a horizontal trading range.

To catch a trend-following move wait for a bearish breakout of the support of the range.

You need at least hourly candle close below.

Then short aggressively or on a retest with your first goal being 0.843 level.

In case of a bullish breakout of the range, the setup will be invalid though.

❤️Please, support this idea with like and comment!❤️