$USCPCEPIMM -U.S PCE (October/2024)ECONOMICS:USCPCEPIMM

October/2024

source: U.S. Bureau of Economic Analysis

-The US core PCE price index, the Federal Reserve’s preferred gauge to measure underlying inflation, rose by 0.3% from the previous month in October 2024, the same pace as in September and matching market forecasts.

Service prices rose by 0.4%, while goods prices decreased 0.1%. Year-on-year, core PCE prices rose by 2.8% in October, the most in six months, also in line with market estimates.

PCE

-United States PCE (October/2024)$USCPCEPEPIMM 0.3%

(October/2024)

source: U.S. Bureau of Economic Analysis

-The US core PCE price index, the Federal Reserve’s preferred gauge to measure underlying inflation, rose by 0.3% from the previous month in September of 2024, the highest gain in five months, following an upwardly revised 0.2% increase in August, matching market forecasts. Service prices rose by 0.3%, while goods prices decreased 0.1%.

Year-on-Year, core PCE prices rose 2.7%, the same as in August, but above forecasts of 2.6%. source: U.S. Bureau of Economic Analysis

RSI Flags Gold Risks Before GDP, PCE Data? Gold is set to face two major US economic data points this week, following last week’s surprise 50-basis-point interest rate cut from the Federal Reserve: U.S. GDP figures on Thursday and Core Personal Consumption Expenditures (PCE) on Friday

Danielle DiMartino Booth of Quill Intelligence argues the Fed’s larger-than-expected cut signals concerns over potential negative GDP revisions, casting doubt on the chances of a “soft landing” for the U.S. economy.

Jerome Powell is also going to be speaking on Thursday at the 2024 U.S. Treasury Market Conference. But his remarks may take a backseat to the data.

The 4-hour Relative Strength Index (RSI) has climbed above 70, signaling overbought conditions and suggesting caution for gold buyers. If the metal turns corrective, the price could test $2,613.

Will the dollar bounce back from its current decline?

The US July PCE was in line with market consensus. Headline PCE prices rose 0.2% from a month ago and 2.5% from a year ago, which aligns with market expectations. Core PCE, the Fed's price benchmark, rose only 0.16%, slower than the previous month's 0.18%. This is the lowest level this year and has catalyzed the market sentiment of the Fed’s rate cut.

It is worth noting that despite a 0.3% increase in personal income, surpassing the previous month's 0.2%, the savings rate remains alarmingly low. This is because personal consumption expenditures are growing at a faster rate than personal income.

The current savings rate has dropped to 2.9%, marking only the second instance in the past 16 years, since the global financial crisis, the savings rate has fallen to the 2% range.

This implies that consumption in the United States could decline quickly, serving as a cautionary signal that if employment falters, there may be insufficient buffers to sustain consumption.

DXY sustained its uptrend after breaking out of the descending channel and advanced to 101.60. The price consolidates around the 101.50-101.70 range, waiting for an additional price trigger.

If the price breaches the resistance at 101.80 while holding above the EMA, the price may gain upward momentum toward 102.60. Conversely, if DXY fails to stay above both EMAs and retreats to the support at 100.50, the price could fall further to the 100.00 threshold.

GBP/USD to Track 100-MA Slope? GBP/USD to Track 100-MA Slope?

On Wednesday, GBP/USD traders will focus on the UK's July Manufacturing and Services PMI, expected to show slight increases.

Although, more significant events will come from the U.S., including the annualized Q2 2024 GDP and the PCE Price Index.

The Fed's preferred inflation gauge likely cooled in June, suggesting its efforts to curb prices are working, potentially paving the way for rate cuts in September.

Markets expect the Fed to maintain the federal funds rate next week but anticipate a cut in September, according to the CME Group's FedWatch tool.

GBP/USD extends the decline from the monthly high (1.3045), pulling the Relative Strength Index (RSI) back from overbought territory. It found support after briefly easing below 1.29 and may track the positive slope in the 100-period SMA.

Market tests BoJ with yen at 1986 low The Japanese yen tumbled beyond 160 per USD, marking its weakest level since 1986. This is a critical threshold that previously prompted intervention by Japanese authorities. In May, Japan depleted a record ¥9.8 trillion to bolster the yen.

Masato Kanda, Tokyo's top currency diplomat, attempted to mitigate the surge above 160.00 with strong verbal interventions, yet he mentioned no specific target level. This ambiguity was perceived by some market participants as a green light to drive the pair to 160.82.

The lack of immediate intervention from the Bank of Japan post-160 breakout raises questions: Does this signal an open path to the next psychological levels?

In June alone, the yen has slipped roughly 1.5% against the dollar, extending its year-to-date decline to about 13%. Should there be a retracement from the previous 160 intervention level, buying interest is expected to resurface around the 158.00 support, aligning with the 38.2% Fibonacci retracement level.

Fundamentally, traders are eyeing tomorrow's US Jobless Claims data, followed by Tokyo CPI and US PCE releases on Friday, which could be critical in shaping the next moves in the yen.

$WMT 10D, $56 incoming, Tower Top BreakdownTower Top Breakdown in the works. Seems like whatever or whenever it happens, it will be close to next Friday. Remain Bearish unless new highs are established. Seemingly easy Trade here. MACD in same positioning as well as RSI. Seems like WMT doesn't get much volume in general. Not necessarily a bad thing. Options could pay well here.

Top USD trades to watch ahead of Core PCE Data release The Federal Reserve’s preferred inflation gauge, US Core PCE (Personal Consumption Expenditure) Price Index MoM, is released at the end of the coming week. This means some USD trades could present themselves.

But first, a quick recap on why the Core PCE Price Index matters and why it is the Fed’s preferred gauge:

Unlike the more familiar Consumer Price Index (CPI), which uses a fixed basket of goods and services, the Core PCE offers a snapshot of consumer spending with a flexible and broader basket of goods and services that adapts to changes in consumer behavior. Importantly, it excludes volatile food and energy prices though. It is thus argued that the Core PCE provides a clearer view of underlying inflation trends.

Some trading opportunities might exist in the EUR/USD and USD/CAD. The Euro Area’s Inflation Rate (Flash) data is due a few hours before US PCE, while Canada’s GDP Growth data is released at the exact same time as US PCE.

GBPUSD Short Fundamental + Technical AnalyzeFundamentals : This weeks GBP PMI coupled with USD Unemployment claims and Core PCE has sent the Dollar rallying while GBP has been in some consolidation until today.

Technical : From a Technical point GBP broke the Bearish Trendline at the same time the Dollar was rallying from news, GBP later retraced some of the sell off and retested the Bearish Trendline it broke earlier which is where the short opportunity become available. Target around a 1% move or check to see when the Dollar takes out its high around 106.5

U.S Core PCE (FEDS FAVOURITE METRIC)U.S Core PCE (FEDS FAVOURITE METRIC)

Rep: 2.8% ✅ Slight decrease as Expected ✅

Exp: 2.8%

Prev: 2.9%

U.S. Headline PCE

Rep: 2.4% ✅ Notable Decrease Expected ✅

Exp: 2.4%

Prev: 2.6%

Both Headline & Core PCE have come in lower and as expected;

✅ Core decreased from 2.9% to 2.8%

✅ Headline PCE decreased from 2.6% to 2.4%

Historical Core PCE Norms

On the chart you can see that since 1990 the typical Core PCE range is between 1 - 3% (red dotted lines on chart - green area). We are slowly getting back down into this more historically moderate level. We have fallen below the 3% level and down into the historically moderate zone for PCE levels.

The Federal Reserve have advised that Core PCE is expected to decline to 2.2% by 2025 & finally reach its 2% target in 2026. At this rate we might reach 2% a little sooner than that.

For the full breakdown of the Core and Headline PCE and to know the differences between PCE and CPI, please review the Macro Monday I previously released which explains it all (see below link).

PUKA

U.S Core PCE Price Index (MoM)ECONOMICS:USCPCEPIMM

Core PCE prices in the US, which exclude food and energy,

rose by 0.2% from the previous month in December of 2023, aligned with market estimates, and picking up slightly from the 0.1% increase in November.

From the previous year,

Core PCE prices edged 2.9% higher,

undershooting market estimates of 3% to mark the lowest reading since February 2021.

The data extended the disinflation trend in prices measured by the Federal Reserve’s preferred gauge, consistent with previous signals of rate cuts to be delivered this year. Regarding the whole national PCE that includes energy and food, prices rose by 0.2% from the prior month and 2.6% from the prior year, consistent with expectations.

Prices for goods rose by less than 0.1% from 2022, while those for services remained elevated at 3.9%.

source: U.S. Bureau of Economic Analysis

edges up as US inflation print fuels Fed rate cut speculation 26 January 2024, 17:04

•EUR/USD rises in North American trading, buoyed by softer US core PCE inflation data.

•Fed's core PCE index fall to 2.9% raises hopes for interest rate cut, aiding EUR/USD's climb.

•Mixed European signals: German consumer confidence falls, Spanish unemployment at 16-year low, ahead of Fed decision.

The EUR/USD gained some 0.14% in early trading during the North American session as prices in the United States (US) remained above the US Federal Reserve’s goal but eased compared to November’s figures. The major trades at 1.0866 after diving to a low of 1.0812.

The Euro got a life-line of a softer US PCE report

The Fed’s preferred gauge for inflation, the Personal Consumption Expenditures (PCE), rose 2.6% in the 12 months to December, as expected on an annual basis, while core PCE dipped from 3.2% to 2.9% and below forecasts. After the data, the EUR/USD climbed sharply and clocked a daily high of 1.0885 before retreating toward current exchange rates, as the data reaffirmed investors' speculations that the Fed could begin cutting rates by the summer.

The CME FedWatch Tool depicts the odds for a quarter of a percentage rate cut by the Fed at 51.4%, while 50 basis points stand at 37.8%. Nevertheless, US Treasury bond yields reversed its course, climbing higher and putting a lid on the EUR/USD rise.

Meanwhile, data across the pond showed that German consumers remain pessimistic amidst economic uncertainty after the GfK Consumer Confidence for February plunged from .25.4 in January to -29.7. In Spain, the Unemployment Rate fell to levels last seen in 2007, from 11.84% to 11.76% in the last quarter of 2023, according to an INE report.

Ahead of the next week, the main spotlight would be the Federal Reserve’s monetary policy decision on January 30-31.

EUR/USD Price Analysis: Technical outlook

Following the US data release, the EUR/USD advanced towards 1.0900 but failed to break yesterday’s high, which could pave the way for a pullback to the 200-day moving average (DMA) at 1.0843. Downside risks are seen at today’s low 1.0812, followed by the 1.0800 figure. Conversely, if buyers lift the spot prices above 1.0900, as they eye the 50-DMA at 1.0920.

U.S. Core PCE Comes in Lower than Expected U.S Core PCE (FEDS FAVOURITE METRIC)

Rep: 2.9% ✅ Lower Than Expected ✅

Exp: 3.0%

Prev: 3.2%

U.S. Headline PCE

Rep: 2.6% ✅ In Line with Expectations ✅

Exp: 2.6%

Prev: 2.6%

Historical Core PCE Norms

On the chart you can see that since 1990 the typical Core PCE range is between 1 - 3% (red dotted lines on chart). We are slowly getting back down into this more historically moderate level. We have just fallen below the 3% level and down into the historically moderate zone for PCE levels.

The Federal Reserve have advised that Core PCE is expected to decline to 2.2% by 2025 & finally reach its 2% target in 2026. At this rate we might reach 2% a little sooner than that.

For the full breakdown of the Core and Headline PCE and to know the differences between PCE and CPI, please review the Macro Monday I previously released which explains it all (in the comments below).

PUKA

USD/JPY shrugs after US GDPThe Japanese yen has edged lower on Thursday. In the North American session, USD/JPY is trading at 147.62, up 0.08%.

The US economy continues to surprise with stronger-than-expected data. On Wednesday, the services and manufacturing PMIs both accelerated and beat the estimates, followed by first-estimate GDP for the fourth quarter earlier today.

The economy sparkled with an expansion of 3.3% q/q, blowing past the consensus estimate of 2.0%. This follows the blowout gain of 4.9% in the third quarter. Consumer spending remained strong at 2.8%, compared to 3.1% in the third quarter. The US economy expanded in 2023 at 2.5% y/y, up from 1.9% in 2022. The US dollar's reaction to the positive GDP report has been muted.

There were concerns earlier this year that the economy might tip into a recession, as the Fed continued to raise interest rates to beat down inflation. However, solid consumer spending and a resilient labour market have boosted economic growth and the Fed is well on its way to achieving the tricky task of a soft landing for the economy.

On the inflation front, the core personal expenditure price index was unchanged at 2% in the fourth quarter, while the headline index rose 1.7%, down sharply from 2.6 in Q3. The week wraps up with the personal consumption expenditures (PCE) price index on Friday, considered the Fed's preferred inflation gauge. The PCE price index and core PCE price index are expected to edge slightly lower in January, which would be an encouraging sign that the inflation is moving lower.

Japan releases Tokyo Core CPI, a key inflation indicator, on Friday. The consensus estimate for January stands at 1.9% y/y for January, after a 2.1% gain in December. If the estimate proves correct, it would mark the first time in almost two years that it has fallen below the BoJ's target of 2%.

USD/JPY is testing resistance at 147.54, followed by resistance at 148.44

There is support at 146.63 and 145.73

Macro Monday 25~The Feds Inflation Barometer – Core PCE Macro Monday 25

The Feds Favorite Inflation Barometer – Core PCE

The US Core Personal Consumption Expenditures (PCE) are released this Friday 22nd December 2023. Currently Core PCE is the most important component to the Federal Reserve in making their interest rate decisions and thus it will provide a great insight into what lies ahead in terms of interest rate policy for Q1 2024.

Known as the Federal Reserve’s favorite gauge for inflation, Core PCE is a crucial economic indicator that provides insights into the general trend in consumer spending (it excludes the more volatile energy & food costs).

Jerome Powell

“I will focus on core PCE inflation, which omits the food and energy components.”

25th Aug 2023

The Bureau of Economic Analysis (BEA) compiles and publishes the Core PCE report which is considered a more comprehensive measure of general trends in consumer spending than some other indicators, such as the Consumer Price Index (CPI).

We will briefly cover the differences between CPI and PCE which will eventually lead us to why specifically the Core PCE is the preferred barometer for inflation (over headline and core CPI and over headline PCE).

Stick with me here and lets have a look at CPI vs PCE first…

CPI Vs PCE - Main differences?

Consumer Price Index: CPI is a metric that follows a fixed basket of goods. This fixed basket of items is measured month to month providing a consistent “basket of goods” cost for the common urban consumer. This allows for the basket of items to remain relatively unchanged thus providing an indication of how costs may be increasing or decreasing for the common consumer using the said basket (the basket is updated but not a frequently as the PCE basket).

Personal Consumption Expenditures: PCE includes a broader range of goods and services, and it is based on more frequent updates to the basket of goods and services that represent consumer spending, thus PCE captures more of the trend or trend changes in consumer spending. PCE includes expenditures on durable goods (e.g., cars and appliances), nondurable goods (e.g., food and clothing), and services (e.g., healthcare and education). This breakdown provides insights into which sectors of the economy are experiencing changes in consumer spending. We covered Durable Goods in a prior Macro Monday (I will link same under the published version on my TradingView). The bottom line on PCE is that it is more broader and more consumer led report thus arguably providing a more accurate indication of the wider spending habits of the consumer

Headline Vs Core (for both CPI and PCE)

In general Headline CPI and Headline PCE have an all-encompassing basket of goods and services included whilst Core CPI and Core PCE focus on a subset by excluding the volatile components of food and energy.

Analysts and policymakers often consider both Headline and Core to gain a comprehensive understanding of inflation trends, however Core PCE in particular provides the deepest and broadest insights into consumer led spending habits and provides the true underlying inflation by removing volatile commodities (Food & Energy). Lets look at CORE PCE a more closely

What is the benefit of excluding food and energy from inflation figures for Core PCE and why is this so beneficial?

1. Reduced Volatility: Energy and food prices are known to be more volatile and subject to temporary fluctuations due to factors such as weather conditions, geopolitical events, and supply chain disruptions. By excluding these components, Core PCE aims to provide a more stable measure of inflation.

2. General Inflation Trend Focus: As noted above, the short-term volatility in energy and food prices can mask the underlying aggregate trend in other goods and services, so the PCE eliminates some of this short term noise from food and energy inflation figures.

3. Captures Persistent Underlying Inflation Forces: Core PCE filters out the impact of temporary shocks to energy and food prices. This can be valuable for assessing whether inflationary pressures are becoming ingrained in the economy in the general sense.

4. Long Term Planning for the Consumer and the Fed: Understanding the underlying inflation trend is crucial to knowing the base level of the cost trend. Core PCE can provide a more reliable gauge for long-term economic planning by smoothing out short-term fluctuations.This provides investors, consumers and the Fed with a sort of long term general expenditure based moving average (the Core PCE) for the underlying inflation burden that is trending in an economy. All three participants can make the necessary adjustments to cater to this long term trajectory and thus the metric is a powerful tool for all involved.

Now that we know why the PCE is such a useful metric we can have a look at the long term PCE chart and see how things have been trending.

For the record CPI already came out for the month of November as CPI is typically released mid-month whilst PCE is released towards the end of the month.

Remember we will have an update this Friday from the BLS on the November readings for Core and Headline PCE, so we can see how we are looking then.

The Core and Headline CPI Chart

This CPI chart illustrates the following:

▫️ You can clearly see how Core CPI is less volatile than Headline CPI. As discussed above, Core CPI removes the volatile food and energy expenditures to provide a more general view of underlying inflation (based on a fixed basket of goods)

▫️ It is clear that we are not at the Federal Reserves target of 2% which is also outlined on the chart (purple line). It is critical to understand that we are still not at or below the target 2% level regardless of the FOMC’s determination of a likely hold on interest rates and reductions to interest rates in 2024. Lets see can the target be met first.

▫️ You can see that since 2002 Core CPI has fluctuated one standard deviation above and below the 2% inflation level between 1% and 3%. It is clear that we are not back into this standardized zone between 1 – 3%.

The Core and Headline PCE Chart (SUBJECT CHART AT TOP PROVIDED TODAY)

(will be updated this with newly released figures this Friday 22nd Dec)

This CPI chart illustrates many of the same findings from the CPI chart above:

▫️ Core PCE provides the deepest and broadest insights into consumer led spending habits versus a more fixed and stringent basket of goods for CPI, making Core PCE the Feds favorite inflation barometer to watch.

▫️ You can clearly see how Core PCE is less volatile than Headline PCE. As discussed above, Core PCE removes the volatile food and energy expenditures to provide a more general view of underlying inflation (based on a fixed basket of goods).

▫️ It is clear that we are not at the Federal Reserve’s target of 2% which is also outlined on the chart (purple line). The Federal Reserve have advised that Core PCE is expected to decline to 2.2% by 2025 & finally reach its 2% target in 2026. Anything that happens to interfere with this between now and then will need to be addressed by the fed.

▫️ You can see that since 1991 Core PCE has fluctuated one standard deviation above and below the 2% inflation level between 1% and 3%. It is clear that we are not back into this standardized zone between 1 – 3%.

Summary

You can visualize on the charts why the Core CPI and Core PCE is more important to Chair Powell, both Core metrics on the charts are almost like a slower moving average providing an indication of the longer term inflation trend. Right now Headline metrics are diving down past the Core metrics and the Federal Reserve cannot just take that volatile headline figure to make long term decisions. The Core PCE/CPI provides the long term trend trajectory whilst the Headline can offer early/lead signals of the direction of inflation, however core must be observed to determine the resilience of the long term trend. Furthermore, Core PCE is perceived by the FED as having more value as it has its finger on the pulse of the consumers spending habits by covering a broader range of expenditures whilst also accounting for consumer led spending trends. The CPI basket of goods in more fixed/restricted in terms of the goods it accounts for. This is why the FED values Core PCE so highly as a versatile and all encompassing gauge of inflation.

Hopefully you’ve come away today with a greater understanding of why the Core CPI and PCE data is preferred by the Fed ahead of headline inflation and also why the Core PCE comes out ahead as the chosen long term inflation gauge.

Any questions or observations, please throw them into the comments and I will be onto them as quickly as possible,

Thanks for reading,

PUKA

EUR/USD rebounds after sharp lossesThe euro has bounced back on Friday after sliding 0.99% a day earlier. In the European session, EUR/USD is trading at 1.1018, up 0.38%. On the economic calendar, the US PCE Price index, the Fed's preferred inflation gauge, fell to 3.0% in June, down from 3.8% in May.

The European Central Bank raised interest rates by 0.25% on Thursday, bringing the main rate to 3.75%. The ECB statement warned that inflation, although on the decline, "is expected to remain too high for too long". The ECB did not provide any forward guidance, as the statement said the Governing Council would base its decisions on the data. ECB President Lagarde didn't add much to this stance, saying that ECB members were "open-minded" about rate decisions at upcoming meetings and wouldn't commit to whether the ECB would raise or pause in September.

The rate increase can be described as a 'hawkish hike', as the statement kept the door open for further hikes. Nevertheless, the euro lost ground following the decision, which could reflect expectations that the ECB is close to its peak rate, despite the hawkish rhetoric.

The eurozone economy is struggling, and this week's Services PMIs pointed to weakness in Germany and France, the biggest economies in the bloc. The eurozone could slip into recession this year, which means that the ECB will have to think carefully before its raises rates. On the other side of the coin, inflation, which is the ECB's number one priority, is at 5.5%, well above the target of 2%. The eurozone releases the July inflation report on Monday and the reading could be a key factor in the ECB's rate decision at the September meeting.

The euro lost further ground on Thursday after better-than-expected US data. In the second quarter, GDP rose 2.4% q/q, above the Q1 reading of 2.0% and the consensus estimate of 1.8%. US Durable Goods Orders and unemployment claims were better than expected, a further indication that the Fed may be able to guide the economy to a soft landing even with interest rates at their highest levels in 22 years.

EUR/USD is testing resistance at 1.1002. The next resistance line is 1.1063

There is support at 1.0895 and close by at 1.0861

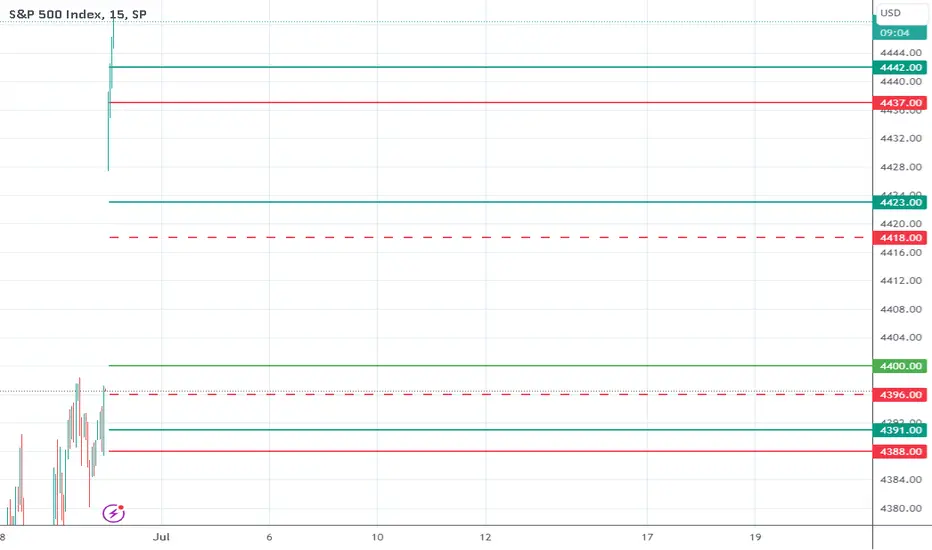

Soft PCE Adding to the Window Dressing Push UpS&P 500 INDEX MODEL TRADING PLANS for FRI. 06/30

The choppy trading for the last week or so appears now resolved to the upside with the soft PCE numbers released this morning. This appears fueling the typical quarter-end window dressing by funds, resulting in the path of least resistance being to the upside. Cover any open shorts and avoid going short - next week's holiday-shortened week could add more spikes to the upside to hit any stops on the shorts.

The previously stated resistance level of 4400-4410 is now the support level. Do not be short while above these levels. With a quarter-point rate hike next week a given, the FOMC meeting next week might become a non-event unless Powell delivers a shocking surprise (which is very unlikely). Hence, this spike up has a potential to turn into the next leg of the bull.

Positional Trading Models: Our positional models' were short at 4350 with a stop at 4416, which was hit this morning for a loss of 66 points. Models are now flat and indicate remaining flat into the weekend.

By definition, positional trading models may carry the positions overnight and over multiple days, and hence assume trading an index-tracking instrument that trades beyond the regular session, with the trailing stops - if any - being active in the overnight session.

Aggressive/Intraday Models: Our aggressive, intraday models indicate the trading plans below for today.

Aggressive, Intraday Trading Plans:

For today, our aggressive intraday models indicate going long on a break above 4442, 4423, 4400, or 4391 with a 9-point trailing stop, and going short on a break below 4437 or 4388 with a 9-point trailing stop.

Models indicate explicit long exits on a break below 4418 or 4396. Models also indicate a break-even hard stop once a trade gets into a 4-point profit level. Models indicate taking these signals from 10:16am EST or later.

By definition the intraday models do not hold any positions overnight - the models exit any open position at the close of the last bar (3:59pm bar or 4:00pm bar, depending on your platform's bar timing convention).

To avoid getting whipsawed, use at least a 5-minute closing or a higher time frame (a 1-minute if you know what you are doing) - depending on your risk tolerance and trading style - to determine the signals.

(WHAT IS THE CREDIBILITY and the PERFORMANCE OF OUR MODEL TRADING PLANS over the LAST WEEK, LAST MONTH, LAST YEAR? Please check for yourself how our pre-published model trades have performed so far! Seeing is believing!)

NOTES - HOW TO INTERPRET/USE THESE TRADING PLANS:

(i) The trading levels identified are derived from our A.I. Powered Quant Models. Depending on the market conditions, these may or may not correspond to any specific indicator(s).

(ii) These trading plans may be used to trade in any instrument that tracks the S&P 500 Index (e.g., ETFs such as SPY, derivatives such as futures and options on futures, and SPX options), triggered by the price levels in the Index. The results of these indicated trades would vary widely depending on the timeframe you use (tick chart, 1 minute, or 5 minute, or 15 minute or 60 minute etc.), the quality of your broker's execution, any slippages, your trading commissions and many other factors.

(iii) These are NOT trading recommendations for any individual(s) and may or may not be suitable to your own financial objectives and risk tolerance - USE these ONLY as educational tools to inform and educate your own trading decisions, at your own risk.

#spx, #spx500, #spy, #sp500, #esmini, #indextrading, #daytrading, #models, #tradingplans, #outlook, #economy, #bear, #yields, #stocks, #futures, #inflation, #recession, #fomc, #fed, #pce, #softpce

Daily Market Analysis - MONDAY JUNE 26, 2023The momentum of stocks is affected by global growth concerns and central bank actions, while the euro experiences an upswing.

Key News:

Eurozone - ECB McCaul Speaks

Eurozone - ECB President Lagarde Speaks

The US stock market is currently experiencing a decline amidst deteriorating global growth forecasts, primarily attributed to weak global Purchasing Managers' Index (PMI) readings. This worrisome trend is particularly prominent in Europe, where the risk of a severe economic downturn is higher compared to the United States. Consequently, the dollar is expected to maintain its support in the short term due to these circumstances.

Throughout this week, stocks have faced unfavorable conditions, resulting in the unraveling of various trades involving large-cap technology companies. Specifically, the Nasdaq index is taking a considerable hit, predominantly due to profit-taking in the artificial intelligence (AI) sector. The prevailing sentiment among investors is to withdraw their profits from AI-related investments, contributing to the downward pressure on the Nasdaq.

Nasdaq daily chart

Looking ahead to the upcoming week, the focus will shift towards a fresh wave of inflation releases following the conclusion of major central bank decisions.

The euro has experienced a robust month, benefiting from the market's anticipation of the European Central Bank (ECB) adopting a more aggressive approach in raising interest rates compared to previous expectations. Despite signs of moderating inflation and sluggish economic activity, the ECB has expressed its intention to pursue higher rates. However, this commitment may carry risks in the long term, potentially limiting the ECB's flexibility in responding to changing economic conditions. Nevertheless, the rally in European yields has made the euro an increasingly attractive investment option for market participants. Furthermore, the weakness observed in the US dollar and the Japanese yen has provided additional support to the euro, as foreign exchange dynamics are often influenced by relative performance.

EUR/USD daily chart

As we look to the future, a critical question arises regarding the momentum of the euro's rally. The answer to this question is likely to be influenced by the forthcoming inflation report scheduled for release on Friday and its implications for the European Central Bank's (ECB) future decisions. Throughout this year, inflation has displayed a consistent downward trend, and recent business surveys indicate that this trend has persisted into June. Notably, selling prices have been rising at the slowest pace in over two years, further contributing to the overall picture of declining inflationary pressures.

In terms of market performance, the DAX index has witnessed a notable decline, predominantly driven by a sharp decrease in the shares of Siemens Energy. The company's stock plummeted by over 30% following its decision to withdraw its full-year guidance due to challenges faced by its Spanish Gamesa operation. This development has had a significant impact on the DAX index's overall performance and has garnered attention from market participants.

DAX daily chart

In a similar vein, the FTSE 100 index has encountered downward pressure, resulting in a decline below the crucial 7,500 level. This descent has brought the index back to levels observed earlier in the trading period, reminiscent of the beginning of the year. The FTSE 100's retreat reflects the prevailing market sentiment and highlights the challenges and uncertainties currently influencing the broader market landscape.

FTSE 100 daily chart

In the United States, the week will commence with the unveiling of significant economic indicators, including durable goods orders and new home sales for the month of May on Tuesday. This will be followed by the release of crucial data on Friday, including the core Personal Consumption Expenditures (PCE) price index, personal consumption, and income figures for the same month.

In recent weeks, there has been a notable back-and-forth between Federal Reserve officials and market participants, resembling a game of chicken. While policymakers have signaled their intention to implement two more interest rate hikes throughout the remainder of the year, investors have only priced in expectations for one. The ultimate determinant of who is right in this scenario will depend on the persistency of inflationary pressures. The outcome will carry implications for the performance of the US dollar, as its value is intricately linked to interest rate differentials and market expectations.

US Dollar Currency Index daily chart

Throughout this month, the US dollar has encountered downward pressure, primarily influenced by two factors. Firstly, there has been market skepticism surrounding the Federal Reserve's hawkish signals, which has created uncertainty among investors. Secondly, the prevailing optimistic sentiment in stock markets has reduced the demand for safe-haven assets, including the US dollar.

Gold, on the other hand, has faced a challenging couple of months as Wall Street anticipates more aggressive tightening measures from central banks across Europe. The strong demand for Treasuries, driven by investor concerns about the global growth outlook, has caused the dollar to rally. However, as the stock market experiences a more pronounced selloff, gold is beginning to attract safe-haven flows. This is evident as gold prices have fallen to the $1920 level, prompting some investors to seek refuge in the precious metal as a hedge against market volatility and uncertainty.

XAU/USD daily chart

Gold received an additional boost when Federal Reserve official Bostic expressed his preference for no further rate hikes for the remainder of the year. This sentiment supported the precious metal's rebound. However, the momentum of the rebound waned when the latest PMI data failed to demonstrate sufficient weakness in the service sector, which would have justified a pause in rate hikes.

Looking ahead, the upcoming week will play a crucial role in shaping expectations regarding future Fed rate hikes. This will be influenced by the release of the Personal Consumption Expenditures (PCE) readings and remarks from Federal Reserve Chair Powell. If market participants, as reflected in swap futures, start to believe that the Fed is likely to implement two more rate increases, gold may remain vulnerable. However, if risk aversion intensifies and investors seek safe-haven assets, gold could experience an influx of buying pressure.

Key support for gold is anticipated at the $1900 level, indicating a price level where buying interest could emerge. On the other hand, resistance is likely to be encountered around the $1960 region, signifying a level where selling pressure may intensify. These levels will be closely monitored by traders and investors as they assess the future trajectory of gold prices.

QQQ Outlook 0626-30/2023Technical Analysis: Last week’s price action put NASDAQ:QQQ back inside the bullish channel we’ve been watching since March. We should see come corrective price action this week before tech runs higher.

Bulls will look to see if we can stay above last week’s lows at 360. It is crucial bulls hold this level or we could see the daily fair value gap that could be filled below at 357.66.

Bears will want to see a breakdown under the daily fair value gap, where we could test the strong monthly level at 354.43. If we lose the levels above, we can look for a test of the lower trendline in the upcoming weeks, and possibly a large gap to fill to the downside from 336.67-332.91. Inside this gap is the 50SMA and the 61.8% retrace at 334.00.

Upside Targets: 364.57 → 370.10 → 373.83 → 380.76 → 386.28

Downside Targets: 360.00 → 358.97 → 357.66 → 354.43 → 352.46

SPY Outlook 06/26-30/2023Last week’s newsletter, we leaned bearish and the market made lower lows 4 out of the 4 trading sessions. With more fed speakers this week, PCE and Consumer Confidence data releases, and political turmoil in Russia, uncertainty can cause volatility in the market bringing down equities.

Technical Analysis:

AMEX:SPY is still due for a retest of the bull flag and daily channel breakout around 429.57. Should this area not hold, a .618 retrace would suggest we pullback to the gap below at 424-423. I do think we revisit that, and possibly test the daily fair value gap below 419.

Bulls will want price action to stay above the weekly 432.03 level. If this holds, we can target the gap above at 437.45-438.97.

Bears will want to try and and break below the red uptrend trendline. If we cannot hold 432.03, we can target the previous bull flag breakout at 429.61. If that doesn’t hold, we could target the 50% retracement where we bullflagged in the beginning of the month around 426.70. An even deeper target is the the daily gap below at 423.95-422.92. Should this gap fill, I would flip long.

Upside Targets: 436.00 → 437.45→ 438.97 → 441.21 → 443.90

Downside Targets: 432.03 → 429.61 → 428.78 → 426.70 → 425.14

GLD Bullish Outlook 06/26-30/2023AMEX:GLD is hot on my watch list as uncertainty in the world markets should cause investors to park their money in gold. AMEX:GLD is down -4% for the quarter and is due for a rebound.

Technical Analysis:

AMEX:GLD has been consolidating in a falling wedge and is approaching the .618 retrace at 177.24.

I lean bullish on AMEX:GLD as long as we don’t break the falling wedge structure and can hold above the gap at 176.18. I am expecting a gap fill to the upside at 181.37.

Bears will want to see this falling wedge invalidate with a gap to fill to the downside at 173.80.

Upside Targets: 178.75 → 179.84 → 181.08 → 181.97 → 183.21

Downside Targets: 177.78 → 176.82 → 176.20 → 174.83 → 174.46

Gold fell to $1955 after Fed MintuesFed Minutes at midnight on Thursday and Fed member's speech deliver a hawkish stance. This hawkish stance may be considering raising interest rates or tightening monetary policy with other tools this next half year to pressure the high inflation and cool down the inflation down to a target rate of 2%. This can lead to a stronger US dollar and higher yields on US Treasury bonds continuously, making gold less attractive as a store of value and investment option.

On Thursday European trading session, the gold failed to break out $1,985 and went down to continue its downtrend, testing the May 23 lowest price of $1,955. Suppose the gold price breakout $1955; the next target would be $1,948 and $1,944 (Red zone). However, the US dollar and the US Treasury yield could soften if the US GDP and PCE data are lower than expected on Friday, and gold price would rebound. Therefore, the resistance may target $1,969 and $1973 in the short run (Blue zone).

DXY Weekly Forecast | 22nd May 2023Fundamental Backdrop

The Flash Manufacturing PMI is expected to decrease from 50.2 to 50.0 which shows contraction in economic health.

The Flash Services PMI is also expected to drop from 53.6 to 52.6.

The FOMC Meeting Minutes on Thursday. The FED will talk about future interest rates which was previously indicated to be on pause.

Technical Confluences

Near-term resistance at 103.500

Next resistance at 105.000

Minor support at 102.765

Major support at 102.200

Idea

With the Flash Manufacturing PMI and Flash Services PMI expected to drop, it could cause the DXY to drop further towards the 102.700 minor support.

If the FED chooses to pause or indicate pausing of interest rates, it can cause the DXY to drop even further towards the 102.200 major support level.

NOT FINANCIAL ADVICE DISCLAIMER

The trading related ideas posted by OlympusLabs are for educational and informational purposes only and should not be considered as financial advice. Trading in financial markets involves a high degree of risk, and individuals should carefully consider their investment objectives, financial situation, and risk tolerance before making any trading decisions based on our ideas.

We are not a licensed financial advisor or professional, and the information we are providing is based on our personal experience and research. We make no guarantees or promises regarding the accuracy, completeness, or reliability of the information provided, and users should do their own research and analysis before making any trades.

Users should be aware that trading involves significant risk, and there is no guarantee of profit. Any trading strategy may result in losses, and individuals should be prepared to accept those risks.

OlympusLabs and its affiliates are not responsible for any losses or damages that may result from the use of our trading related ideas or the information provided on our platform. Users should seek the advice of a licensed financial advisor or professional if they have any doubts or concerns about their investment strategies.