Nsestocks

RELIANCE - Elliott wave analysis - WXY correction The complex correction WXY is in progress, where Y is about to start correcting as ABC. Wait for impulse drop, which will confirm the Y wave down. Then short the bounce for more down side up to 1680.

Plz give a like if you agree with EW count.

ICICIBank - Elliott wave analysis - corrective down It is in ABC zigzag correction down after completing ABC zigzag up sequence. C wave may be going to extend as further impulse. So corrective bounce of 2nd of C wave will be short sell set up.

Plz give a like if you agree with EW count.

Grasim - Elliott wave analysis - 4th wave correction It is in 4th wave correction and possibly it will be sharp correction ABC down. It may go up to 1100 level to correct the 4th wave, which is again a buy zone for final 5th wave up.

Plz give a like if you agree with EW count.

Eichermot - Elliott wave analysis - ABC zigzag up & double topIt is in corrective cycle after completing ABC zigzag cycle in 4 hr time frame. It correcting down as double top pattern and achieved the target zone. There is a chance of small bounc now.

Plz give a like if you agree with EW count.

Nifty - Elliott wave analysis - correction The correction ABC is under progress. Nifty is in C wave corrective cycle. It is possible to extend the correction down side.

Plz give a like if you agree with EW count.

Punjab National BankThe stock analysis was carried out on Feb 9 in response to a question asked on a social media platform and thereafter it has rallied. Read the reasons behind the pick below.

PNB shares appear to be the better option amongst PSU Banks.

Reasons supporting the pick:

1. Second largest PSU Bank in terms of market capitalisation.

2. PNB’s merger with United Bank of India and Oriental Bank of Commerce has improved the PAT (profit after tax) for three straight quarters of FY21 i.e 538 cr. in Q1, 576 cr. in Q2 and 747 cr. in Q3. NII has been improved by over 80% on a YoY basis for Q3.

3. FII’s holding has increased from ~1% to ~4% which signals a strong bullish bias towards the bank. Huge volumes of shares are being traded for close to 7 trading sessions

4. Government of India’s emphasis on Privatisation of PSU’s will leave a lesser count of PSU Banks in India and PNB is expected to remain on the PSU Bankside.

5. Stock is trading/consolidating in a lifetime low trajectory of 26–39 for close to a year now. The all-time high of the stock is 279.8 which is far away from the current levels. Therefore keeping the range of 26–39 as a strong base, the stock has only one way to move i.e up.

6. Technically speaking, the stock is trading at 0.64 times its book value and appears to be undervalued given the above-mentioned reasons.

The stock has a strong resistance zone at 40.55–42.80 and a strong support zone at 32.50-34.50 levels and hence perfect time to invest would be when the price is close to the support level or breaks the resistance zone i.e above 42.80.

The first target for the stock would be 53+ and the second target would be 70+ in months to come.

Refer to the chart for levels.

Invest and forget, it might give some surprising returns.

NOTE: These findings and levels are purely based upon the knowledge and understanding of the post publisher. The idea here is to predict the future price movements hence, please do not consider this as stock advice or recommendation.

PNB - Punjab National BankResearch pick:

Reasons supporting the pick:

1. Second largest PSU Bank in terms of market capitalisation.

2. PNB’s merger with United Bank of India and Oriental Bank of Commerce has improved the PAT (profit after tax) for three straight quarters of FY21 i.e ₹ 538 crores in Q1, ₹ 576 crores in Q2 and ₹ 747 crores in Q3. NII has been improved over 80% on a YoY basis for Q3.

3. FII’s holding has increased from ~1% to ~4% which signals a strong bullish bias towards the bank. Huge volumes of shares are being traded for close to 7 trading sessions

4. Government of India’s emphasis on Privatisation of PSU’s will leave a lesser count of PSU Banks in India and PNB is expected to remain on the PSU Bankside.

5. Stock is trading/consolidating in a lifetime low trajectory of 26–39 for close to a year now. The all-time high of the stock is 279.8 which is far away from the current levels. Therefore keeping the range of 26–39 as a strong base, the stock has only one way to move i.e up.

6. Technically speaking, the stock is trading at 0.64 times its book value and appears to be undervalued given the above-mentioned reasons.

Talking about targets (Daily time frame):

The stock has a strong resistance zone at 40 .55–42.80 and a strong support zone at 32.50-34.50 levels and hence perfect time to invest would be when the price is close to the support level or breaks the resistance zone i.e above 42.80.

The first target for the stock would be 53+ and the second target would be 70+ in months to come.

NOTE: These findings and levels are purely based upon the knowledge and understanding of the post publisher. The idea here is to predict the future price movements hence, please do not consider this as stock advice or recommendation.

HPCL - HINDPETRO HP NSE:HINDPETRO CL had been consolidating close to a year now. And by looking at the pace of recovery of the Indian economy and keeping the earnings season in mind, HPCL seems to be ready for an up move. Price levels are as below -

Buy - ~ 212 + ( stock respects the support level of 210 )

Target - 235+

SL - 208

Influencing factors -

1. Budget expectations

2. Earnings for 3rd quarter for FY 21

3. Increase in the demand of automobile and its ancillaries.

NOTE : These findings and levels are purely based upon the knowledge and understanding of the post publisher. The idea here is to predict the future price movements hence, please do not consider this as a stock advice or recommendation.

Tatamotors - Elliott wave analysis - 4th wave correction It is in 4th wave correction, which is expected to be zigzag abc down to complete it before it start running up in 5th wave.

Reliance - Elliott wave analysis - ABC correction of Y downIt is in B wave of Y wave down in double zigzag down cycle. Go short on bounce for C of Y wave down.

LT - Elliott wave analysis - Correction down It looks like completed the major impulse up cycle and now correction is in progress. Go short if break the top range consolidation downside.

Grasim - Elliott wave analysis - 3rd wave about to endIt is in strong uptrend and one more high is expected to finish to 3rd wave of the cycle. The correction will start only after that for 4th wave.

Gail - Elliott wave analysis - ABC correction It is in corrective mode after completing the impulse cycle. Go short on bounce of X wave for Y wave down.

Drreddy - Elliott wave analysis - ABC correction It was doing what exactly expected in earlier updates. The B wave is in progress and may go upside before it starts running down for C wave of corrective cycle.

Coalindia - Elliott wave analysis - C wave upIt is in C wave up in ABC zigzag cycle. The 5th wave up of C will start soon. It is either completing C wave or 1st wave of C wave. We will know when it start correcting the move.

Adaniport - Elliott wave analysis - 4th wave correctionIt completed the 3rd wave impulse up and now expected to correct down as 4th wave.

1900 LIMIT ORDER PLACED Reliance Industries Daily and Weekly time frames looking good for long term in terms of Price Action

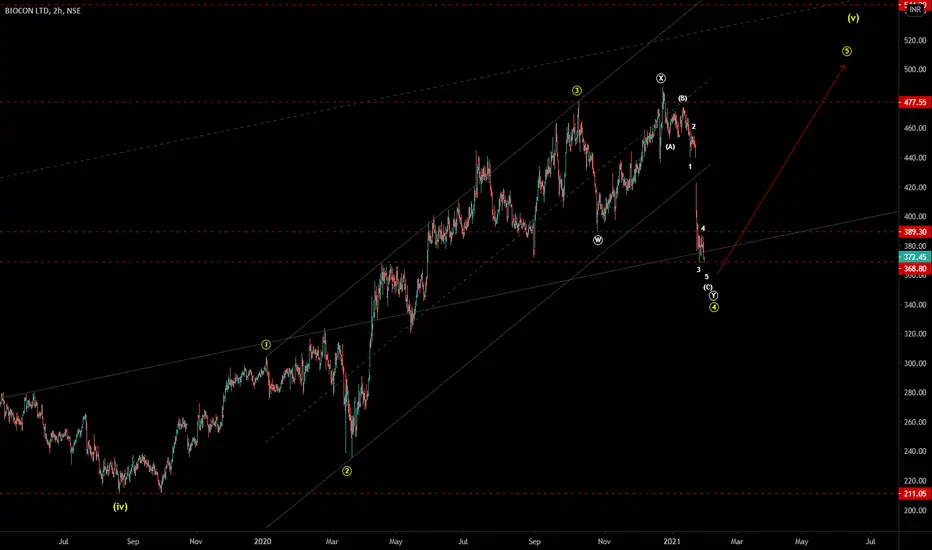

BIOCON - Elliott wave analysis - 5th wave up It is about to finish the correction of 4th wave as WXY cycle. After a new low it should bounce to confirm the cycle. Buy only in 2nd wave correction after confirming the 1st wave impulse. The target of the trade will be above 550.

RELIANCE - Elliott wave analysis - ABC of Y wave down It completed the X wave as ABC correction. The Y wave will unfold in ABC too, where B wave will start soon to correct the move. Short sell when B wave finished for C Wave down as final move of Y wave.

LT - Elliott wave analysis - Correction down It is about to reverse down after completing Ending diagonal structure of the cycle. The short sell set up will triggered only when it break the level below 1325. The target zone for trade will be around 1215-1150.