GBPUSD to Continue Sinking Lower The price action of the GBPUSD is busy developing a new downtrend, following FED's January policy decision and the better-than-expected GDP numbers in the U.S. for Q4.

The downtrend is taking the form of a 1-5 impulse wave pattern, as postulated by the Elliott Wave Theory.

Following the decisive breakdown below the 61.8 per cent Fibonacci retracement level at 1.33867 and lower limit of the descending channel, the price action is now likely to head towards the previous swing low at 1.32000.

GDP

A Big Turning Point for USDCNHin the past few years, USDCNH usually found a turning point in the 1st Q, especially around the Chinese New Year.

Today there is a big rally in USDCNH.

Reuters report, FX conversion before the week-long Lunar New Year holiday, which starts on Jan. 31, has been traditionally heavier as exporters need to settle their dollar receipts for goods payments and employee bonuses, but markets widely expect some weakness could kick in soon.

www.reuters.com

Fed signal a rate hike in March and PBoC is going to keep monetary policy neutral to slightly loose, this will narrow the rate spread of these two currencies and favor more dollar strengthening.

China's GDP will still have pressure this year as the Q4 GDP slowed to 4% in Q4 2021.

The 20th National Congress of the Communist Party of China will be held in the second half of this year likely in Oct or Nov, the Chinese government will be busy with political issues. Will, there be any further pressure on the economy, we need to wait and see.

a surge in USDCNH on 27 Jan 2022, should show a bottom of this pairs of currency and head for 6.5-6.65 in coming months.

TOTAL MARKET CAP - GarbageIn an unregulated space where digital numbers are sold to the people with USDT and unregulated stable coins - While the US overthrows nations that try to issue their own currencies or nationalize their resources - Here we have the GDPs of dozens of developing nations being absorbed within hours by so called "whales"... Only whales I am seeing are corrupt US officials who work as puppets in a space that can't regulate Tether but will send its troops in to fight and let innocent people die if a rival economy ever tried to do the same thing..

This shit is out of hand... In two months the amount that came flooding out of this market could have ended global malnutrition 6x based on the figured the World Bank and UN give... Bogus

Dji/Gdp A look are Dji comapred to GdpI hate writing in this the chart explains it self. no predictions needed.

Pound shrugs off sharp UK dataThe British pound has posted very slight gains on Friday. In the European session, GBP/USD is trading at 1.3720, up 0.09% on the day.

The pound is yawning despite better than expected UK data today. GDP jumped 0.9% m/m in November, above the consensus of 0.4%, while Manufacturing Production rose 1.1% m/m, crushing the estimate of 0.2%. Both readings were above the October releases, indicating that the UK recovery continues. GDP for Q4 is expected to reach or surpass the pre-Covid level (Q4 2019), barring a disappointing December GDP report.

We continue to see a rotation out of US dollars this week, with the British pound and other majors racking up impressive gains of around 1 percent. The driver behind the US dollar's weakness has been elevated risk appetite, which has not waned despite exploding Omicron cases, a soft nonfarm payrolls report and a hawkish Federal Reserve. The markets appear to have an answer for all of these developments. The Omicron wave has not wreaked havoc on the global economy, US wage growth is strong, and Fed Chair Jerome Powell is confident that red-hot inflation in the US will ease during the year. Still, risk sentiment can change quickly, and I would not be surprised to see a US dollar comeback in the near term if Omicron is more damaging than anticipated or if inflation heads even higher.

Prime Minister Boris Johnson is under intense criticism after revelations that his staff held parties during the height of the Covid lockdowns. One party was apparently held the night before the funeral of Queen Elizabeth's husband, and a poignant photo of the Queen sitting alone during the funeral has made Party-Gate look even worse. The latest political crisis has not made a dent in the pound's upswing, perhaps because Johnson is no stranger to controversy or an indication that investors are more concerned about inflation and omicron rather than partying at 10 Downing Street.

There are support lines at 1.3482 and 1.3372.

GBP/USD continues to test resistance at 1.3708. This is followed by resistance at 1.3818

GDP Growth / Macro Economic Commentary - Forecast 2022

The Macro Trend for 2022 for the 6th consecutive year remains - Aggression for every Point on the Curve.

__________________________________________________________________________________________

Commodity Hoarding to the Space Race to Territorial Disputes, 2022 will be a remarkable year for the

Rising Dragon.

One of more interesting but non-topics has been the Velocity with which China has demonstrated their

intent o assert dominance - Space.

Plans to Inhabitat the Southern Pole of the Moon have been moved forward 10 years, from 2035 to 2025.

Why is this remotely significant?

Excellent question.

It provides for the colonization of the Moon as well as its weaponization.

Water, Platinum, Rare Earths, Titanium, Oxygen, hydrogen, and Immense Solar Power are abundant.

Two items of interest caught my attention in reading through their forward Plans:

1. A large 1 Megawatt Nuclear Reactor

2. A large Mass - Rail Accelerator

By the time Blue Origin and Space Prime intend to attempt a planned mission to the South Polar region of the

Moon - the welcome mat will have been rolled up.

The Space Wars will begin ahead of 2024.

China is seeking dominance within the interior of the Solar System within the decade while CERN fiddles with

every larger experiments here on Earth 175 Meters below the surface.

As James T. would utter - "Space the Final Frontier"

How else does a World Power collateralize the Future... it ain't here.

_______________________________________________________________________________________________

Commodity Hoarding has been well underway in the Land of the CCP for 6 straight years.

Slowly, methodically - China has been amassing resources at a pace unparalleled in Human History.

I'm quite certain, it is not for nothing, mixed metaphors aside.

Stockpiling / Inflation Hedging

Global Food prices in 2021 increased 30.127%

Wassup CP Lie

3% gains month over month... Wheat and Oils were up significantly in 2021.

Money Supply increases Globally were up 27.14%

51% of the World's Grains belong to China.

Relying on Supply Chains?

Foolish.

20.12% of the Worlds Population has 51+% of its grains. 60% of Rice and 51% of Wheat.

Clearly, the CCP is front running higher Inflation.

Intertest Hedge - Had you purchased MRE's or Survival Foods in Dried Form... Congratulations,

you outperformed the S&P 500 by a large margin. Gold / Silver, you would have crushed by a

factor of 20X. 2012 Au Average Price ~ $1,668.86 while in 2022 it is $1,798.89.

Silver - we won't bother, a clear loser by an enormous margin. YArd relics in the Age of REAL

RETURNS.

Bonds - If you enjoy Net Negative REAL RETURNS - Load up.

You can't eat Door Stops or Paper which Provide your capital being sent asymptotically to ZERO

in Purchasing Power Parity in 11.37 Year - this is using the Bullshit Data, in REAL Terms at 2021

rates of REAL RETURNS - yeah, it's less than 3.4 Years.

Speaking of Supply Chains prior to the Reality of PPP, China is claiming Fisheries in Asia and the South

Pacific with rather large swaths of Net.

Who's going to stop them? The land of Oz... unlikely - they're too busy being enormous knee benders.

Japan?

Unlikely.

The Philippines?

There aren't enough shoes in Imelda's closet to throw at them?

The United States?

Every simulation I've seen shows the United States is crushed in War Games in the South China Sea.

Biden's bellicose rhetoric only pissed them off and accelerated their aggressions.

Taiwan... 50 years later, the United States of America acknowledges it is a Territory of China.

Bradon isn't going to stop them from taking what we have long permitted to occur.

Doubt it?

See Hong Kong.

_______________________________________________________________________________________________

Resource Wars which accelerated in 2021 will only increase in both Scope and Scale in 2022.

Something to consider prior to getting encouraged about illusory Gains.

We are facing daunting changes most Americans will struggle to accept.

Squander.

Apathy is the Glove into which Evil slips its Hand.

_______________________________________________________________________________________________

I began 2022 with Rainbows and Butterflies and Compromise...

The Dragon isn't "Toothless" and we aren't going to "Train" him.

Liechtenstein, Luxembourg, Monaco, and Singapore are the residences

of the level pullers, well out of the way.

_______________________________________________________________________________________________

20% Gains in 2021 for the NQ & ES is not sustainable.

Fed Policy is changing in a few months

VX for 2021 held a number of Flash Crashes.

Instability.

VAX Variants and boosts... creating effectiveness panics.

Real Estate in China remains a Large Risk end of January during the Lunar New Year.

$212 Billion in Balance SHeet... Sh_t. M&A won't prop this Junk Up.

Deflating Real Estate in China is De Facto, CCP is no better than the FED... hard to believe,

but they are indeed worse.

3.7 Million Speculators in the US joined the likes of BTC, ETH, and DOGE - most are

underwater HODLings.

Shiba - the Hope Coin... Tokens for Tulips, the Greatest Fools.

NFT''s - the Hot Air Ballon for Buyers, give it a few years. JPEGs have zero Intrinsic Value.

Too much $ chasing Submariners to Oysters... Tick Tock... it's a clock, I've got one on my

phone.

Bubble troubles are everywhere.

The Genius of Bull Markets... is not Genius at all, it is simply a freakout.

5 Variant of Covid, a new one in China over the weekend, right in time for the Lunacy New Year.

Het your booster Jab before it's too late... oops, another Variant -XIan

A news Cycle filled with Mania and Setups.

Trave Restrictions and Camping with Covid are in Trend.

Germany, the Congo degenerates are waiting on head wrappings for far higher energy prices

in the fatherland... Putin enjoying the NATO Squeeze as it fits the return of NatGAs from the

Pipes to Poland.

Energy will be one of the more Volatile Instruments to Trade in 2022.

Buckle up, Sporty is an understatement.

Yen dips despite stronger JPY retail salesThe Japanese yen continues to lose ground. The yen suffered a third straight losing week, and the trend has continued on Monday. With USD/JPY currently trading around the 114.70 level, the 115 line is vulnerable. The pair last breached this symbolic level a month ago, but the dollar couldn't consolidate above this level.

Japan's retail sales overperforms

Christmas week started off on a positive note, as Japan Retail Sales for November posted a strong gain of 1.9% y/y, ahead of the consensus of 1.7% and above the 0.9% gain in October. Consumers were out in force as Covid-19 cases fell during November. Still, the Omicron variant has started to spread in Japan's major cities, leading to fears that the government could impose health restrictions or that consumers will stay at home to avoid contracting Omicron.

Japan is set on spending its way to a stronger economy, and parliament approved a record 10.8 trillion yen budget on Friday, which includes payouts to households and businesses hit by Covid. Japan's economy is expected to roar back in Q4, with a consensus of 6.4% growth, after a contraction of -3.6% in the third quarter.

Inflation is on the rise in Japan. In November, Core CPI rose 0.5% y/y, above the consensus of 0.4%. That might seem insignificant compared with inflation numbers in the UK and the United States, but given that inflation has been negligible for years in Japan, this is certainly a change in direction. The uptick in inflation will be welcome news at the Bank of Japan, and should ease policymakers' concerns about deflation. The bank's inflation target of 2% remains a long way off, but inflation could move higher if the Omicron does not derail economic activity.

USD/JPY is putting pressure on resistance at 114.82. Above, there is resistance at 115.26

There is support at 113.65 and 112.90

Canadian dollar buoyed by risk sentimentThe Omicron variant continues to rage through Europe and the US, but the markets are in a positive mood. Why? There is a feeling that Omicron is much milder than Delta, which means that a wave of Omicron may get a lot of people sick, but it will not kill thousands and overload hospitals with severely ill patients. Time will tell if this is an accurate diagnosis. In the meantime, the global recovery outlook has improved and commodity prices are higher, which is good news for the Canadian dollar.

Risk sentiment has been moving up and down over the past few weeks, depending on the headlines de jour concerning Omicron. Investors have been encouraged by the latest medical reports out of the UK and elsewhere which indicate that Omicron is up to 70% less severe than Delta. The equity markets continue to rise and risk barometers such as the Canadian dollar have moved higher this week.

The markets are starting to view Omicron like a storm in a tea cup, but there is good reason not to sigh in relief just yet. First, Omicron is five times more contagious than Delta, which means that unvaccinated people could experience severe symptoms. Second, some reports indicate that Omicron is not necessarily less severe than Delta. Third, the Chinese Sinovac vaccine, which is the only one available for a majority of the world (the developing countries), doesn't appear to be effective against Omicron. In the meantime, the markets have dismissed Omicron as an annoying nuisance, and this rosy outlook could continue into January, barring some grim statistics from a wave of Omicron.

Canada's GDP for October rebounded with a gain of 0.8% y/y, up nicely from 0.1% beforehand. The economy has now expanded for five straight months and the BoC is projecting growth in Q4 at 4.0% y/y, as the economy continues to gather steam, despite the challenges of Covid.

USD/CAD has support at 1.2756. Below, there is support at 1.2615

There is resistance at 1.2987. Above, there is resistance at 1.3077

Will GDP lift the loonie?The Canadian dollar is trading quietly ahead of the release of Canada's GDP for October later today. The loonie took advantage of broad US weakness on Wednesday, posting gains of 0.53%, its best daily showing since December 7th.

Canada's economy was stagnant in September, with a paltry gain of 0.1%. October, however, is expected to show a strong rebound. Statistics Canada is projecting a gain of 0.8% m/m, but some solid data since this projection has added upside risk, which could translate into a gain of 1.0%. I would expect a GDP reading of 0.8% or higher to provide a boost for the Canadian dollar.

A strong GDP report could also have an impact on the Bank of Canada, which has signalled that it plans to embark on a series of hikes in 2022 (a much faster pace than the Fed). A rate hike is widely expected in Q1 2022, but the date of lift-off remains uncertain and will likely be determined by the strength of economic indicators. April is the most likely date at the present time, but an acceleration in the October GDP and higher inflation could push that date forward, perhaps as early as January.

There is a lot of uncertainty surrounding the Omicron variant, and the screaming headlines continue to impact risk appetite as well as risk barometers such as the Canadian dollar. The currency slid 1.3% last week, as Omicron raged across Europe and the US, raising fears of new health restrictions and possible lockdowns. Risk sentiment has rebounded sharply this week, as more reports show that although Omicron is much more contagious than Delta, the symptoms have been less severe. The positive news has sent the Canadian dollar higher this week.

The roller-coaster in the currency markets could well continue for the rest of December, as the markets are being driven by headline volatility rather than market trends. Therefore, caution in these turbulent, illiquid markets is strongly recommended.

USD/CAD has support at 1.2756. Below, there is support at 1.2615

There is resistance at 1.2987. Above, there is resistance at 1.3077

Pound higher despite GDP revisionThe UK economy grew 1.1% in the third quarter, revised downwards from the initial estimate of 1.3%. The expansion was led by robust consumer spending, which beat expectations with a gain of 2.7% as lockdowns were lifted in July.

Investors didn't seem perturbed from the downward revision, as the British pound has moved higher today. Still, it's doubtful that fourth-quarter growth will be as strong as Q3. The explosion in cases of the Omicron variant in December has prompted the government to implement plan B, which has dampened the economy, especially the hospitality sector.

There was some light in the pre-Christmas gloom after Prime Minister Boris Johnson announced that it would not introduce new restrictions before Christmas. Still, Johnson warned that there could be further measures after the holiday. This would likely mean limits on the number of people meeting in indoor venues.

With the holiday season comes illiquid markets, which means that market direction will be dictated by headlines, which could translate into volatility. The government announcement of no further restrictions before Christmas certainly removes some uncertainty for market participants, but if infection rates continue to soar in the UK, investors could get jittery and seek the safety of the US dollar at the expense of the pound.

The newest vaccines and pills in the fight against Covid make the headlines daily, but a report about a super-vaccine could shake up the markets if confirmed. According to the report, researchers at Walter Reed Army Institute of Research are testing a vaccine that would protect against all Covid variants. Such a discovery would clearly be a game-changer, and would likely restore risk appetite, which has fallen sharply as Omicron rages across Europe and the US.

GBP/USD has support at 1.3190 and 1.3116

There is resistance at 1.3314 and 1.3364

Pound yawns after data dumpThe British pound has had a rather sleepy week, and the lack of activity has continued in Friday trade, as GBP/USD is hovering at the 1.32 line.

It has been a light calendar week for the UK, and today's data dump didn't have any effect on the drifting pound. The GDP report for September came in at 4.6% y/y, well short of the consensus of 6.6%. Manufacturing Production for September y/y slowed to 1.3%, shy of the forecast of 1.7%. Investors shrugged off the underperforming data, perhaps because they are more focused on two burning issues, Omicron and the BoE rate decision next week.

Omicron has caused some roller-coaster movement in the financial markets. There was a panic in late November, but risk sentiment than rebounded on reports that the variant was less severe than Delta. The World Health Organisation has said that it will have more data on Omicron in a couple of weeks. Although the symptoms appear to be relatively mild, Omicron is up to four times more contagious than Delta, and that has governments worried.

The UK has responded by implementing 'Plan B', which includes some health restrictions, such as wearing masks at public venues. Omicron is spreading quickly across the UK, and it's unclear if Plan B will be enough to control the pandemic. The new health restrictions will likely cut into December/January holiday shopping and stoke inflation, as many shops will raise prices. We can expect a downgrade to Q1 2022 growth forecasts, and the wobbly pound will likely face further headwinds in the New Year.

The BoE holds its policy meeting next week, and whether the bank will press the rate trigger remains up in the air. The markets have priced in a 40% likelihood of a rate hike, making this a live meeting which could have a strong impact on the struggling British pound. The Omicron crisis has dampened the likelihood of a rate hike, and it was noteworthy that Michael Saunders, a hawkish member of the MPC, has stated that it may be prudent to hold off until we have more data about Omicron. If the markets have learned anything from last month's shocker, when the BoE didn't raise rates, it is not to make any assumptions when it comes to Andrew Bailey & Company.

GBP/USD has support at 1.3161 and 1.3091

There is resistance at 1.3336 and 1.3441

What's preventing AUSSIE from climbing further ?Current RISK ON mood in the markets should likely propel AUDUSD higher as the economies around the globe try to recover. As china is dependent heavily on Australia on trade matters, we have every reason to believe that the AUSSIE will likely gain ground as the recovery in the Chinese exports continue.

So from technical point of view, the question that arises is: what is stopping the AUDUSD from climbing further?

Just have a look at the main chart to understand the clear picture. Aussie seems to be supported by a ascending trendline and until this breaks, we are still in an uptrend. Now for this uptrend to resume we need to see clear breakout of the price outside its triangle (descending trendline) to target the next resistance at 0.77700. Lets see how this all plays out!

EXTRA: have a look at the related link section. there is an active SHORT SWING EURGBP WEEKLY TRADE. The entry price is at an excellent level. enter at your own risk if you wish. the analysis is also present behind this trade

THIS JUST REPRESENTS MY ANALYSIS ON THIS PAIR AND ITS NOT A TRADE SIGNAL. I HAVE MANY PAIRS THAT I MONITOR AND ALL OF MY TRADES ARE ON W, D , 4H TIMEFRAME (SWING TRADES). ITS NOT POSSIBLE TO POST ALL OF MY ANALYSIS HERE, HOWEVER I POST TRADE SIGNALS WHEN THE CRITERIA IS MET ON THE FX PAIRS I MONITOR. FOLLOW & LIKE TO RECEIVE FREE FX SWING TRADE SIGNALS CHEERS

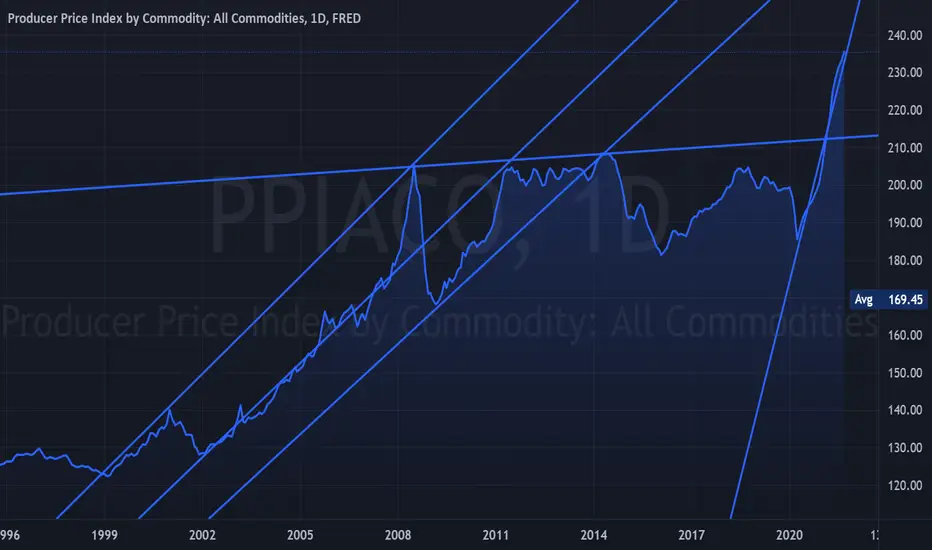

Commodities - Accumulation in Inflation Expectations ContinuingThe "Price" of the "Things We Need" in Trend is quite clear.

Golden Age of the Inflationary Depression is asserting itself

in a clear, concise, and undeniable Thrush.

GDP has been Mis-Reported by 10 - 30% consistently.

___________________________________________________

The Financial Economy has two Halves - one contributes to financing

the real economy, the other does not.

GDP Finance and non-GDP finance.

GDP Finance includes:

Loans for funding real-economic investment and other expenditures

Firm's equity and debt

Taxes

Social Security

Contributions and government bonds to finance public spending

___________________________________________________

Non-GDP Finances include:

Inter Alia - Secondary trading in shares, Bonds & Equities

Real estate as Capital Investment

Trading in Derivatives and Forex

___________________________________________________

Quantity is not Quality - Inflation is a very real Distortion to

Economic and Financial Well Being.

The Golden Bullflag breakoutWelcome back traders to another weekly view on gold,

Gold is in excellent bullish form and is about to go vertical towards my 1870 target. The weekly closing price has nullified the chances for a retest of 1745, with bulls fortifying their gains 1771+ (23.6 fibo). Now the invalidation price for gold bulls moves up to 1770. Meaning a retest of 1770 is still possible and a break below it will break the current bullish structure. As a matter of fact, gold bulls broke the 2 year weekly bullflag with a weekly candle. This is starting to look like the start of something amazing. Let's analyse this baby.

📊 US GDP

Two very volatile weeks are coming at us in full speed. We have the US GDP next Tuesday planned with a forecasted 3.5% GDP growth. There are rumours on the street who are whispering 0.5% GDP growth in Q3, which basically means the economy flatlined. Hard to guess numbers on this one, but what is sure, is that the GDP is pulling back from 6%. Chinese GDP last week disappointed also with the lowest growth since the start of the pandemic. As I explained before, this is extremely bullish for gold.

🔊 FOMC November 2021

The next risk event follows up rapidly on November 3rd with Powell set to announce the start of tapering, which is very bearish for gold. Whether that they will start in November 15th or December 1st, this day will be a big day in the market that will give direction for some time with gold set to retest the 1720-1725 level and its weekly bullflag breakout.

🔮 Cesaro's Crystal Ball

Current rally has similarities with the start of the rally in spring 2021. I see gold breaking the triple top at 1830 and then go back to make a double bottom at 1720. The Daily & Weekly RSI closed 50+, stochastic RSI is in strong bullish momentum & an H4 golden cross is there to function as a cushion. I expect to see 1840 and 1850 in extension before the end of month with the US GDP to be the fundamental trigger.

Trading remains an art of probabilities and the probabilities are high that the FOMC November meeting will be a reason for gold bears to show their strength. Ofcourse gold can keep blasting up from 1875, but I will keep an eye on that 50 fibo level at 1875 and I expect a strong bearish hostile take over from there to test bullish commitments and their bullflag breakout. Depending on the fundamental situation, bears might break through 1720 & 1680 aiming for 1650. Or... Gold bottoms at 1720, with bulls defending their bullflag breakout and we are heading for the 2000 break after.

Cheers,

Cesaro

Gold - Long Pre Inflation DataWe see Gold continuing to move higher whilst it remains above support at $1773. Gold has sustained it's upward momentum on the back of fears surrounding rising inflation and also a weakening US dollar. The precious metal is perceived as an effective hedge against rising inflation as it is seen as a store of value. We await key economic data releases including the Q3 US GDP growth rate on Thursday and the PCE Price Index YoY on Friday for any significant price action.

Atom Prediction ATOM/BTCIn this prediction i will show my prediction to you on ATOM/BTC

which might go up and hit resistance

Gold's weekly Bearish triangle (Update 2)Goodday traders, I hope you are enjoying your weekend with your friends and loves ones.

A massive $35 dollar red candle is what gold printed on the last day of the week, pushed fundamentally by the better than expected retail sales data. The candle is engulfing, massive and full with almost no wick on the downside. This signals the presence of sellers from the 1800 psychological pricelevel after Thursday's hanging man candle, and it shows there will be some 'more pain before more gain' for the yellow shiny metal.

📑 FOMC MInutes

Minutes of the Fed’s September meeting confirmed this week that a tapering of stimulus is all but certain to start this year, although policymakers are sharply divided over inflation and what they should do about it. This in part can also be explained to be bullish for precious metals as investors flock to hedge their risks before the announcement in November, but this need to materialize in the coming weeks.

📊 US GDP October 26th

After the NFP, CPI & FOMC Minutes, the next risk event will be the US GDP data release on October 26th. After Goldman Sachs lowered their GDP forecast for a 3rd straight month, it is expected that the US will print a much lower GDP than previously assumed. This is obviously extremely bullish for gold as I mentioned before (stagflation), but before the GDP data I expect to see a higher low around 1740-1745.

📉 Technicals

Technically I expect to see a bullish retrace now and I want to see price action around the 1780-1785 pricezone, since the H4 50 SMA support still intact. There is still a chance we see 1810 before the dump to 1745 and it all depends if gold bulls can reclaim the important 1780-1785 pricezone, but in normal circumstances I expect the price to continue falling from that level towards 1740-1745. If the bullish defenseline fails, expect much bigger losses towards 1700.

All to be played out in the last 2 weeks of this month.

Cheers,

Cesaro

I'm buying weakness in Chilean stocksAfter the IPCC's recent report showing that the North Atlantic Current may be on its last legs, I decided that I needed to diversify away from the US and Europe a bit. (If the North Atlantic Current fails, it would cause massive, disruptive climate change for Europe and North America.) So I committed to look for opportunities in some country ETFs.

The one I've been buying is $ECH, the iShares Chile ETF. Chile stocks are beaten down because of currency weakness amid heavy pandemic spending, but honestly their debt-to-GDP ratio is still one of the world's best at just 27%. (Contrast the US at 107% and Japan at 238%.)

Chile has had a highly effective vaccine rollout, with the world's sixth highest vaccination rate. (With 67.2% of Chileans fully vaccinated, they lag behind a few much smaller countries, like Malta and Iceland.)

Thanks to pandemic UBI and a high vaccination rate, Fitch yesterday raised its 2021 real GDP growth forecast for Chile from 6.1% to 8.3%, making Chile one of the world's fastest growing economies this year, trailing just behind China's 8.4%. But whereas China ETFs trade at 14x cash flow and yield 1.1%, $ECH trades at less than 5x cash flow with a distribution yield of 2.34%.

There is, undoubtedly, some political risk when buying a Latin American ETF. Latin America is notorious for its political instability, and Chile is no exception. Chile currently ranks 19th in the world for economic freedom, and its current leader is a Harvard-trained economist and business engineer. But he's also wildly unpopular due to excessive use of force against protesters the last couple years. The country is currently in the process of drafting a new national constitution, and many of the constitutional delegates lean left. It remains to be seen what shape the future government of Chile might take.

Despite the uncertainty, the immediate future for Chile looks relatively bright. At this valuation and with this GDP growth rate, I've bought a modest stake and plan to hold for the forseeable future.

GBP/JPY Signal - GBP GDP Data - 13 Oct 2021GBPJPY is trending to the upside currently prior to the GBP Gross Domestic Product data, which measures the total value of all goods and services produced domestically. Technically the pair has broken above the key 154 level, and the RSI is holding bullish levels. We anticipate continued upside into 155.50.

Silver - Short Below Key Resistance We hold a short view on Silver whilst it remains below key resistance at $22.2 despite it's rebound today. The precious metal has been in a downtrend since mid June as the FED indicated a more hawkish stance on monetary policy causing the US dollar to strengthen. Additionally, yields have been rising with the 10 year treasury note yield rising from 1.3% to 1.5% over the past week putting further pressure on Silver prices. We await US GDP growth rate, jobless claims and GDP price index releases this afternoon for any significant price action.

usdcad analysisIn the short term, there is an uptrend that is resisting at 1.27.

In the 1 hour time frame, there is a downward trend that started on September 20 and this trend continues due to the formation of successive H and L.

The downtrend will continue unless the price can cross the resistance level of 1.273.

Data on Canada's PMI and GDP will be released on Friday. This data is very important for the currency pair because it can have a direct impact on the value of the Canadian dollar against the US dollar.

In a period of 15 minutes, a triangular pattern is seen

However, in the downtrend, the price is likely to continue to the main level of 1.26 and then 1.258.

The stop loss in these transactions will be more than 1.273

Pound pushes above 1.38, GDP nextThe British pound has punched above the 1.38 level in the Thursday session. GBP/USD is currently trading at 1.3858, up 0.63% on the day.

After posting three straight days of losses, the British pound has rebounded strongly on Thursday. The US dollar is in retreat against the majors, despite a positive unemployment claims release earlier in the day. Claims fell to 310 thousand, down from 345 thousand a week earlier.

We'll get another look at US inflation data on Friday, with the release of PPI for August expected to indicate that inflation remains red-hot. The consensus stands at 6.5% (YoY) compared to 6.2% in July. The Federal Reserve continues to insist that the surge in inflation is transitory and has been reluctant to respond with a tightening of policy, fearing that the time is not ripe for a scaling back of QE. Still, more investors are sure to join the skeptics if inflation continues to remain at high levels in the final months of 2021.

In the UK, the markets will be treated to a data dump on Friday. The key events are GDP and Manufacturing Production. With the Delta variant of Covid continuing to hurt economic growth, July GDP is expected somewhere around zero, which could mean a small decline. Manufacturing Production is also expected to be sluggish with a forecast of 0.1% (MoM). We could see some strong movement from the pound, depending on the performance of these two releases.

There is resistance at 1.3924. Above, there is resistance at 1.3988, just below the symbolic line of 1.40.

On the downside, we have support at 1.3763 and 1.3666